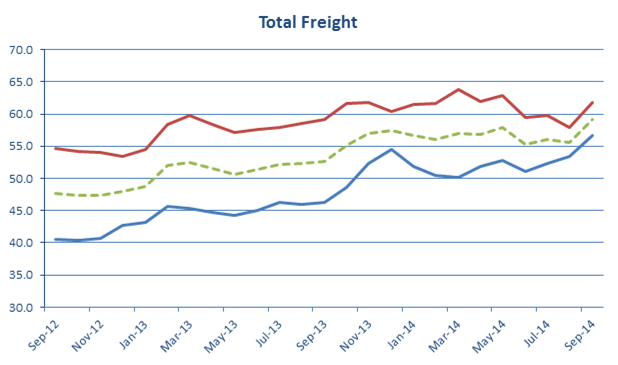

The Stifel Logistics Confidence Index increased at its fastest pace in September, climbing 3.5 points from August to 59.2. Both the present and expected situations noted healthy gains increasing 3.2 and 3.9 points to 56.7 and 61.8 respectively.

Increasing confidence in the global economy appears to be driving these strong gains. As noted in the chart below, the present situation has improved each month since July. Meanwhile, the expected situation remains high despite a few monthly bumps this year.

Airfreight

The overall airfreight logistics confidence index improved 2.9 points to 55.7. The expected situation increased 3.7 points to 58.4 while the present situation increased 2.1 points to 53.0. By trade lane, results were mixed for the present situation with the US lanes declining2.8 from Europe and declining 0.1 to Europe. However, it was the Asia to Europe lane that drove much of the gain for the overall present situation, increasing 8.1 points to 59.6. Could this be attributed to the recent Apple iPhone 6 announcement? Rumors are that the company bought quite a bit of air cargo space, thus blocking competitors from utilizing airfreight.

Still, even July airfreight data indicated a good month, particularly for Asia carriers. These carriers recorded an increase of 7.1% year-over-year, the biggest since the start of 2013.

The expected situation jumped 3.7 points to 58.4. All lanes noted increases with Europe to the US noting the biggest increase of 5.5 points to 57.9.

Sea Freight

The overall Sea freight index increased 4.2 points to 62.7. The expected and present situations increased over 4.0 points as well. All trade lanes reported positive gains for the months. But, of all the trade lanes, Asia to Europe noted the biggest increase for both expected and present situations, 5.6 and 6.2 point gains to 69.2 and 66.5 respectively.

Monthly Question

In this month’s survey, we asked participants, compared with three years ago, have there been any changes in volumes on lanes with their origin/destination in Europe or the US? The majority of participants, 46.6%, indicated there have been increases while 26.0% indicated declines. Meanwhile, 13.7% noted volumes had remained the same while 13.7% indicated they did not have operations on these lanes.

Of the comments, perhaps the most telling concerned declines in freight. One participant indicated “Shipments with Europe as origin have decreased significantly due to the high cost of operating manufacturing in Europe”. While another participant noted “The volumes on lanes from both Europe /Us experienced three years ago was drastically decreased, compare to eight to ten years past”.

More Air Cargo

Alaska Air profit forecast signals rebound from Max woes