posted by AJOT | Mar 04 2015 at 07:50 AM | Liner Shipping

Over the last seven months oil prices have fallen more than most people had thought possible a year ago. As bunker prices are closely correlated with oil prices, a similarly large drop has been seen here. This has led many industry commentators, SeaIntel included, to speculate whether the carriers will speed up their services again, as slowsteaming and super-slow-steaming was instituted when the oil prices increased rapidly. In this week’s Sunday Spotlight, SeaIntel has analysed the cost of speeding up services on Asia-Europe and the Transpacific.

When the carriers slow down the vessels, bunker consumption falls, but as the vessels are sailing slower, more vessels are needed to cover the same distance. If the bunker oil saving is greater than the financing/operational costs of adding a vessel, then it makes sense to slow down, and if vessel costs outweigh bunker costs, it should make sense to speed up.

COO and Partner in SeaIntel, Alan Murphy says: “A number of positive effects would come from speeding up the services. Firstly, it would cut transit times, reduce the shippers’ inventory costs and make the carriers’ products more attractive. Secondly, it would free up some of the carriers’ largest vessels, and make it possible to cascade smaller vessels into trades where they are more suitable. This would be a particularly attractive option for carriers who don’t have enough large vessels. Thirdly, it would give the carriers the option of handing back charter vessels to the ship-owners and hence saving on charter expenses. The last two could also be viewed negatively from the perspective of the industry as a whole, as sudden release of tonnage would naturally add to the endemic overcapacity situation.” A highly complex calculation is required to determine whether services should be speeded up and the result is very sensitive to a number of factors, including the exact deployed vessels on the service, roundtrip distance, fuel efficiency, equivalency charter rates, etc. SeaIntel has therefore decided to base the analysis on three actual, named services in deployment today, rather than finding the speed-up point for a generic service, as this would just add unnecessary complexity to the calculation.

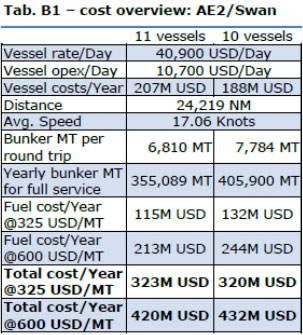

In the Asia-North Europe trade lane SeaIntel analysed the potential for 2M’s AE2/Swan service. By estimating the vessels bunker consumption and taking chartering costs and the vessels’ operational expenses into account SeaIntel has estimated the cost for operating the service at a bunker price of 325 USD per metric tonnes (MT) and 600 USD per MT. A current average bunker price of 325 USD/MT means that the carriers would have to spend 115M USD each year on fuel alone for this service. In July, when the average bunker price was 600 USD/Mt, theyearly bunker oil bill would have been 213M USD. With the current oil prices and vessel expenses the carriers cost are 322M USD a year. If the bunker price was 600 USD/Mt the combined figure would have been 420M USD as shown in the table.

If SeaIntel speeds up the service so the round trip is only 10 weeks, but all other factors are kept equal, bunker consumption increases due to the higher speed required. With an average fuel price of 325 USD/Mt, the fuel expense increases to 132M USD, and would be 244M USD if the bunker price were to jump back up to 600 USD/MT. The carriers would however save 19M USD per year on vessel expenses, by having to deploy one vessel less.

SeaIntel’s analysis shows that with a bunker price of 325 USD/MT the carriers could potentially save 2.3m USD per year on speeding up their services again in the Asia-North Europe trade lane. However, it should be mentioned that the Danish research firm have singled out one service, and there is a chance that it is not representative of the market as a whole.

Even though that the carriers might be able to save money at the moment there are some other factors that should be taken into account before the carriers start speeding up their services.

“It requires considerable time, effort and money to redesign and implement a new network, finding new berthing slots and communicating new transit and cut-off times to customers; it is simply not worth it if the carrier does not expect a long- term gain from such a restructure. Slow-steaming happened exactly because the carriers expected the long term future to be one of high or growing bunker oil prices”, added Mr. Murphy

As the relatively small gains are predicated on a sustained low bunker price - a very uncertain assumption - it is very unlikely that we will see an industry-wide speed up of services, as the network restructuring costs would probably outweigh the potential gains.

SeaIntel also note that, if the carriers started to speed up services massively, that would result in a significant amount of vessels without immediate employment. This would lead to extra capacity in the market, and, as analysed in issue 194 of the Sunday Spotlight, could have a detrimental effect in the trades where capacity is cascaded, and the possibility that freight rates would start tumbling down.

More Liner Shipping

MSC collaborates with GSBN to trial integrated safe transportation certification verification process

Guidi appointment as CMA CGM Italy General Manager

• Paolo Guidi has been appointed as CMA CGM Italy General Manager, effective 1st of May 2024, replacing Romain Vigneaux, former general manager Italy. • Paolo Guidi comes from CMA…