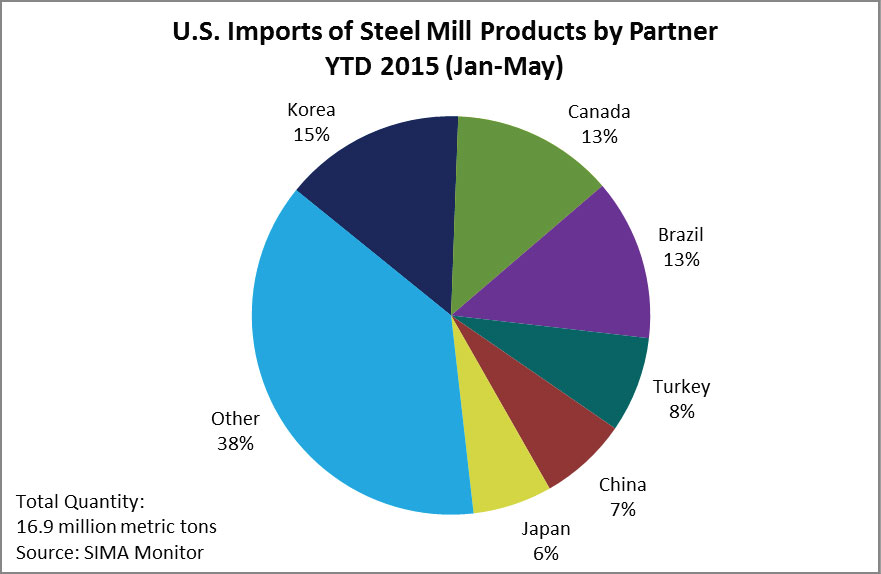

US falls to number two on 17% drop as EU takes top slot. Is a scrap steel export rebound in the cards?

The European Union became the world’s leading exporter of steel scrap in 2014 following an almost negligible increase of 0.3 percent to 17 million tons. Overseas shipments from the United States, meanwhile, tumbled 17.1% to 15.3 million tons, dropping the U.S. to the number two exporter slot last year.

Those were some of the statistics included in the recently-released “World Steel Recycling in Figures” from the Bureau of International Recycling (BIR). The report revealed that steel scrap usage in global steel production climbed 0.9 percent last year to 585 million tons. In all, over 97 million tons of scrap steel were traded across international borders in 2014, according to the BIR.

The strengthening of the U.S. dollar, making U.S. export prices less competitive overseas, was the main factor cited by analysts for the drop in U.S. exports. Most of the scrap that would otherwise have been exported, they also noted, was absorbed by the U.S. domestic market, an additional three million tons, compared to the loss of 3.2 million tons in exports.

China Imports Down 42%

Other reasons for the decrease in U.S. exports include the continuing drop in prices of iron ore, making refinement of steel from ore more attractive. China and other countries such as Turkey have reduced their imports of steel scrap, relying instead more on domestic sources, analysts also note, and Chinese steel mills have come to rely more on ore than on recycled steel as inputs for their operations.

According to “World Steel Recycling in Figures,” a number of countries scaled back their ferrous scrap imports in 2014. Among them, China was down 1.9 million tonnes, or a whopping 42.6%; South Korea was down by 1.2 million tons, 13.6%; Turkey, down 650,000 tons 3.2%; and Taiwan was down by 180,000 tonnes, or 4.1%.

Of these, only Turkey’s steel production dropped in 2014, but much less than its reduction in scrap imports. All four countries are generating and collecting more ferrous scrap internally and are becoming less reliant on imports, at least for now. Three of the top 10 importing countries bought more ferrous scrap in 2014 than in 2013: Thailand, which was up 44%, India, and the United States. Some analysts believe that China and South Korea are moving towards becoming steel scrap exporters over the coming years, although that opinion is not unanimous.

From 2010 through 2013, according to the BIR, Turkey was the largest importer of steel scrap, and the U.S. was the largest exporter. Those two facts existed in symbiosis, as Turkish mills purchased considerable tonnage from shippers on the U.S. East Coast.

Two elements coincided to help weaken this connection. Turkish mills have been focusing on sourcing more scrap domestically, so that overall import levels actually peaked in 2012. As the U.S. dollar strengthened throughout 2014, mill buyers in Turkey and elsewhere began to look to the EU for many of their purchases.

The result, according to the BIR, was that the EU’s export volume in 2014 closely matched 2013’s level: 16.86 million tons in 2014 versus 16.81 million tons in 2013, while exports from the U.S. tanked, dropping the U.S. to second place on the global steel scrap exporter list.

Will Scrap Steel Demand Grow? For the global scrap market to retain its energy, the world steel industry will need to continue to grow. Figures released by the WSA (World Steel Association) show global crude steel output rising over the past five years, although growth in output between 2013 and 2014 grew by only one percent, thanks to the slowdown of China’s economy and the resulting stabilization of that country’s steel output.

Edwin Basson, director general of the World Steel Association, believes that steel output, and the demand for steel scrap, will also grow over the next five years. “I am quite positive about the health of the steel industry,” he said.

Basson estimates that global demand for ferrous scrap for steelmaking will increase by around 110 million tons from 2014 to 2019, driven by China and Turkey, as well as by the Asia-Pacific and NAFTA regions.

Basson believes that the leveling off of output in China’s steel industry may not have a large impact on the global scrap market, nor does he see China becoming a net exporter of ferrous scrap. “Although China will generate more ferrous scrap through end-of-life vehicles and appliances and increased demolition activity,” he said, “Chinese melt shops will use this scrap as part of their raw material mix.” China’s rapid urbanization has affected long-term steel demand in the previous 15 years, Basson concluded, and urbanization in other parts of the world will keep steel demand robust for the next 25 years.

Currency Impact

The big question in the scrap steel market is whether the EU can retain the crown this year. The first quarter of 2015 was a bearish one for steel scrap recyclers worldwide. “There isn’t any scrap around,” said George Adams, CEO of SA Recycling in Orange, California. “Volumes tended to drop off following a sharp fall in prices” such as that seen in the first quarter.

Buyers of scrap watch currency fluctuations and will be making the purchasing decisions that will make the difference in the EU versus U.S. rivalry. Some observers say that the strength of the U.S. dollar has peaked, or is about to, which augurs well for U.S. scrap exporters.

Peter Buxbaum has been writing about international trade and transportation, as well as security, defense, technology, and foreign policy, for over 20 years. Besides contributing to the AJOT, Buxbaum’s work has appeared in such leading publications as Fortune, Forbes, Chief Executive, Computerworld, and Jane’s Defence Weekly. He was educated at Columbia University.