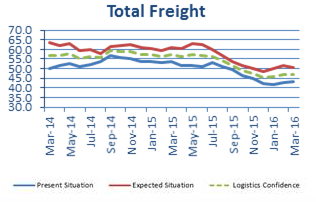

London, UK - Despite improved results in January and February, the March edition of the Stifel Logistics Confidence Index suggests that these months may have merely amounted to positive blips within a downward trend.

The release of February trade volume figures for China showed that the country has experienced significant declines in both imports and exports, with the latter contracting 25.4% year on year; the steepest decline since May 2009.

At the beginning of March, Alphaliner reported that the global fleet of idle container ships reached a six year high, demonstrating the lengths to which carriers are being forced to go in order to cull capacity. This news came as question marks were raised over the feasibility of increases in the size of container vessels.

Research by Drewry found that increasing the size of ships to a capacity of 24,000 TEUs would have a net negative effect upon the industry; requiring significant infrastructure investments at ports and the Suez Canal. The largest containerships at present are Mediterranean Shipping Company’s 19,224 TEU Oscar class vessels, which were introduced in 2015. In the words of Drewry’s Managing Director, “The terminal costs go up and they offset the savings that the shipping lines make.”

In air freight, IATA released statistics for January showing that monthly demand had risen by 2.7%, though available capacity increased by 7%, resulting in a 1.8% contraction in average load factors. The head of the organisation stated that, "It is good news that volumes are growing, but yields and revenues are still under tremendous pressure."

A story of particular significance with regards to air freight was Amazon’s confirmation of a rumoured air cargo venture. The company will lease 20 Boeing 767 jets from Air Transportation Services Group on contracts of five to seven years, and as part of the deal, has an option to acquire 19.9% of ATSG’s shares at a set price during the next five years.

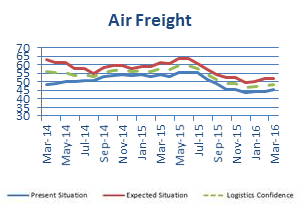

Air freight

The total air freight logistics confidence Index gained 0.5 points in March 2016, totalling 48.6. The Index is 9.3 points lower than in March 2015, and 7.3 points lower than in March 2014. Regarding the present situation, the air freight Index rose by 0.9 points to 45.4.

Continuing on from January, all lanes posted month on month growth with the exception of Asia to Europe, which lost 2.5 points to reach 41.4. Europe to Asia gained 1.3 points, though remained below the 50 point mark, standing at 39.1. US to Europe gained 2.6 points to 49.0, whilst Europe to US also gained 2.6 points, and at 53.0 represented the only lane in positive territory.

In the expected outlook, the total results were flat, as half the lanes saw gains, whilst the other half saw declines. Europe to US recorded the most significant gain, increasing by 2.6 points to 52.2. By contrast, US to Europe fell 1.6 points to 53.3. Meanwhile, Europe to Asia fell by 1.6 points to 49.7, whilst Asia to Europe increased by 0.6 points to 51.8.

Sea Freight

The logistics confidence Index for sea freight declined by 1.0 points to 45.3. Additionally, when compared with the same month in 2015, the Index is 11.4 points lower, and it is also 12.7 points lower than in March 2014.

For the present situation, the Index gained 0.8 points to 41.5. Half of the lanes noted gains, whilst half saw declines. The former group was made up of Europe to US and US to Europe, which noted gains of 3.9 points to 49.3 and 0.9 points to 37.9, respectively.

The expected situation Index for sea freight saw a 2.8 point decline to 49.1, with contractions in all lanes apart from Europe to US, which gained 0.8 points to 56.0. Meanwhile, US to Europe lost 4.6 points, falling to 46.2. Europe to Asia lost 3.0 points, and Asia to Europe declined 4.3 points, with each amounting to 44.1 and 50.5, respectively.

One-Off Question

Each month, respondents to the Stifel Logistics Confidence Index survey are asked a unique, one-off question. The March one-off question referenced both the seasonal dip in air and sea freight volumes derived from Chinese New Year, and the current slowdown of China’s economy. The question asked respondents what they expected to see happen to volumes during this February’s Chinese New Year.

In response, 55% of survey participants, a clear majority, replied that they expected a more pronounced dip than usual, whilst 17% responded to the contrary. The remaining 28% of respondents indicated an expectation that the volume dip would be consistent with historic trends.

To share your thoughts with Stifel and take part in this month’s survey: https://www.surveymonkey.co.uk/r/StifelApr16

More Air Cargo

CMA CGM PSS02 - from Asia to West Africa

CMA CGM informs its customers of the following Peak Season Surcharge (PSS02):

Ryanair CEO urges leadership continuity at Boeing in crisis

Ryanair Holdings Plc Chief Executive Officer Michael O’Leary said Boeing Co. management needs to focus on continuity as it seeks to stabilise the business, and that the new head of…

Airlines must now pay automatic refunds for canceled flights

Airlines will now have to provide automatic refunds to travelers if their flights are canceled or significantly altered under new US Department of Transportation rules.

Japan Airlines CEO describes weak yen as a ‘big problem’

Japan’s weak currency is a “big problem,” Japan Airlines Co. Chief Executive Officer Mitsuko Tottori said in a group interview, adding that a stronger rate than the current level of…