Drewry: The mysterious absence of service cuts

posted by AJOT | Oct 30 2017 at 08:33 AM | Maritime | Liner Shipping

Despite ongoing freight rate erosion, carriers are yet to announce any service suspensions for the slack season. Might this jeopardise any annual contract gains?

Last week Drewry conducted a webinar that provided an overview of our outlook for the container market.

One of the cornerstones of our assessment that carriers will improve profitability next year in spite of a heavy burden of new ships is that we expected them to demonstrate the same level of capacity management skills as they have in the recent past.

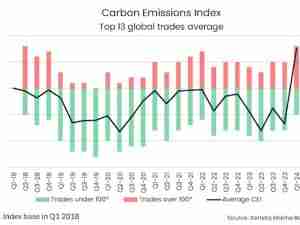

However, even at this very early stage we are starting to be concerned that we might have given them too much credit. The reason for this hesitancy is that lines have for some unapparent reason suddenly eschewed some of their normal modus operandi. In particular, there has been a complete lack of service suspension announcements for the traditional shipping slack season in the fourth and first quarters.

That would be understandable if demand and freight rates were strong, but that isn’t the case now as spot prices on the East-West trading routes have been on a downwards spiral for a number of months. This situation is most significant in the Asia-Europe corridor where annual contract negotiations are already underway. Every weekly deflation to spot rates further weakens carriers’ negotiating position.