Of the four trade lanes covered by the Index, Europe to US reversed is recent performance gains, and across all categories (air and sea, present and expected situation), recorded notable declines. By contrast, the other trade lanes performed well on the whole, with Asia to Europe in particular displaying a considerable month on month improvement. Given the results of previous January editions of the Stifel Index, seasonal uptick in performance is to be generally expected, particularly in the scores for the present situation, and so it may well be that the improvement measured for January 2016 is merely temporary.

Indeed, the view from shipping analysts Drewry is that: “Insufficient measures to reduce ship capacity will lead to an acceleration of freight rate reductions and industry-wide losses in 2016”, with capacity continuing to grow faster than demand. This perspective is corroborated by Alphaliner, who calculated that 24% of total carrier orders in 2015 were composed of ultra-large container vessels, each having a capacity of 18,000 to 22,000 TEU. This will result in further cascading effects, and put greater pressure upon port facilities; an effect observed when the 18,000 TEU CMA-CGM Benjamin Franklin docked at the Port of Los Angeles, with the facility recording a preparation time of two weeks to be able to unload the vessel – such a procedure usually takes two to three days.

With regards to air freight, the picture is less clear. According to the organisation’s predictions for 2016, IATA expects global shipping demand to increase by 3%, up from 1.9% in 2015. Significantly, this gain is below the IMF’s latest projection for global GDP growth; a rate of 3.56%, as per the October 2015 World Economic Outlook. The slowdown in China’s economy is also expected to have a significant impact upon the air freight industry. Another story to watch is Amazon’s apparent move into air freight, which could prove salient in the long-run, though as yet, its importance is uncertain.

Air freight

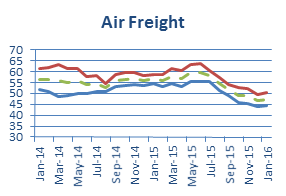

The total air freight logistics confidence Index gained 0.6 points in January 2016, amounting to 47.2. The Index is 9.4 points lower than in January 2015, and 9.3 points lower than in January 2014.

Regarding the present situation, the air freight Index rose by 0.4 points to 44.2. In a reversal of recent trends, all lanes posted month on month growth with the exception of Europe to US, which lost 5.6 points to reach 51.8. By contrast, US to Europe stood at 45.7 after gaining 3.1 points, whilst Asia to Europe and Europe to Asia rose 1.8 and 2.1 points respectively, totaling 43.1 and 36.9.

In the expected outlook, the picture was very similar. Again, Europe to US fell against the previous month, this time losing 5.4 points to 48.8. US to Europe, by contrast, increased by 3.5 points to 52.7, whilst Asia to Europe gained 3.4 points to 50.3. Europe to Asia noted the weakest gain out of the three improved lanes, with a rise of 1.9 points taking the score to 49.3.

Sea Freight

The logistics confidence Index for sea freight improved by 0.3 points to 44.6. Regardless, when compared with the same month in 2015, the Index is 13.4 points lower, and it is also 12.2 points lower than in January 2014.

For the present situation, the Index continued to fall, losing 1.1 points to 39.6. Europe to US represented the poorest performing of the lanes, losing 6.3 points to 48.7. Similarly, US to Europe lost 4.4 points to 36.0. Asia to Europe achieved the best gains with a 3.4 point increase to 39.5 from December, whilst Europe to Asia gained 1.9 points to 34.8.

The expected situation Index for sea freight achieved an overall gain of 1.6 to 49.5, thanks to increases in three lanes. The exception amongst the lanes was Europe to US, which lost 2.6 points to total 54.3. The greatest increase was recorded by Asia to Europe, which rose 4.9 points to 52.7. US to Europe followed, with a gain of 2.3 points taking this lane to 45.0, whilst Europe to Asia rose 1.1 points to 45.8.

One-Off Question

Each month, respondents to the Stifel Logistics Confidence Index survey are asked a unique, one-off question. The January one-off question cited the environment of low capacity and poor profitability in the container shipping industry to ask respondents what they believed to be the main motivation behind CMA CGM’s acquisition of NOL.

The most popular response, with 35% of votes, was that the deal was motivated by market share growth. The next largest response segment was that the deal was intended to strengthen pricing via consolidation; this accounted for 26% of responses. A further 18% of participants believed the main motivation to be the adding of new lanes and a strengthening of density where the shipping line was previously weak. Of the remainder, 9% stated it was to strengthen a hold on key trade lanes, whilst 12% selected ‘other’ reasons.

More Air Cargo

Solar groups lobby Biden to head off sector-roiling trade case