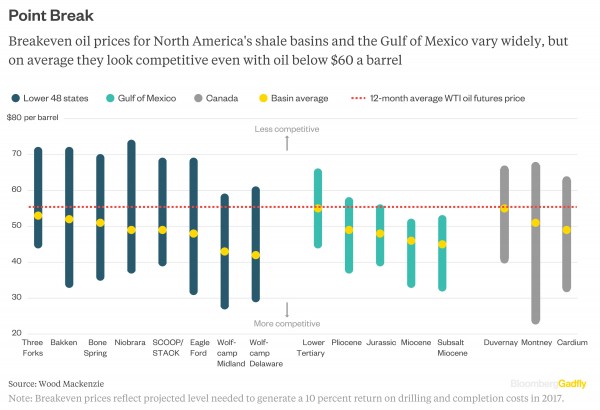

This is not a chart that OPEC would like:

It shows Wood Mackenzie’s projections of breakeven oil prices for new wells in North America’s shale basins and the Gulf of Mexico. The first thing to notice is that, on average, it makes sense on paper to drill almost anywhere.Reality is a bit more complicated. As we discussed in this earlier column, all-in costs for exploration and production companies include things like general and administrative overhead and interest charges, all of which must be borne by the barrels they produce. In addition, transportation costs can vary widely depending on where you’re drilling, where your refining customers are and whether the oil is being shipped by pipeline, rail-car or truck.

Average North American Shale Breakeven Price: < $50 A Barrel

So consider a driller in the Bakken with an average breakeven price of $52 a barrel. Add in, say, $4 for overhead and interest charges and assume the oil is being sent from North Dakota to refiners on the Gulf Coast by railroad at $12 a barrel. The all-in breakeven price for that barrel is $68. If there’s space on a pipeline available, then that comes down to maybe $63 (which is why President Trump’s push for new pipelines is welcomed particularly by inland drillers).

In contrast, drillers in the Wolfcamp basin—part of the prolific Permian basin—enjoy average breakeven prices of about $42 to $43 a barrel on Wood Mackenzie’s projections. Add in $4 of overhead and interest but only $3 to ship the oil across Texas, and the all-in breakeven price is about $50. No wonder the Permian shale is the hottest area for E&P investment.

Go back to the chart, and the other thing to notice is the wide range of breakeven prices. The average for the shale basins is $32 a barrel. Not everyone gets those lower average economics.

Even if the message is a mixed one, though, it is still unwelcome to OPEC. Only a few years ago, breakeven prices in shale basins were estimated to be north of $80 a barrel or, for some, $100. On Wood MacKenzie’s numbers, even the upper end of the range is now in the low $70s.

Even if suffering oilfield-services contractors demand higher fees and help raise those breakeven prices some, OPEC’s room to maneuver in using supply cuts to push prices higher has shrunk significantly.

The short time that it takes to develop shale resources, relative to conventional oilfields, and the E&P industry’s ability to raise money on the back of promises of growth mean that pushing the price too high could unleash another round of fighting for market share, just as we’ve seen these past two years.

And this time, that danger zone isn’t $100-plus, but more like $60 or $70-plus. Oil bulls watching today’s spot price of $54 may well think that’s just fine—although that would ignore the inherent volatility of a scenario where shale and OPEC are battling it out.

As for many of OPEC’s members, their economies just aren’t built to survive on the prospect of (maybe) $70 a barrel. Therein lies a real wildcard in the years to come.

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.