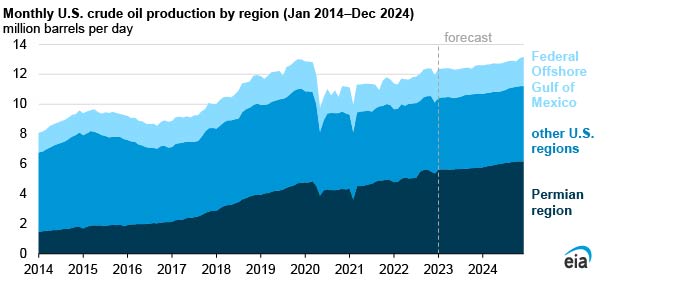

In our January 2023 Short-Term Energy Outlook, we forecast that crude oil production in the United States will average 12.4 million barrels per day (b/d) in 2023 and 12.8 million b/d in 2024, surpassing the previous record of 12.3 million b/d set in 2019. In 2022, U.S. crude oil production averaged an estimated 11.9 million b/d. Increased production in the Permian region and, to a lesser extent, in the Federal Offshore Gulf of Mexico (GOM) drives our forecast growth in production. We base our forecast on our expectations of crude oil prices and infrastructure capacity additions.

Our forecast of crude oil production in the Permian increases by 470,000 b/d to average 5.7 million b/d in 2023. Completion of new natural gas pipelines will allow producers to transport more of the natural gas that is produced along with crude oil (associated natural gas) to market, removing a potential constraint on crude oil production. Producers currently flare some of the natural gas they produce. We forecast that crude oil production in the GOM will increase by 120,000 b/d in 2023, while production in other regions of the United States (except for the Permian) declines slightly.

In 2024, we forecast that crude oil production in the Permian will increase by 350,000 b/d, while production in the GOM declines slightly. We forecast that production in other U.S. crude oil-producing regions increases by 70,000 b/d in 2024.

We forecast the U.S. benchmark West Texas Intermediate (WTI) crude oil price will average $77 per barrel (b) in 2023 and $72/b in 2024, down from $95/b in 2022. Despite declining crude oil prices, we expect the WTI price will remain high enough to support crude oil production growth, especially in the Permian, where data from the Dallas Fed Energy Survey indicate that average breakeven prices range from $50/b to $54/b.