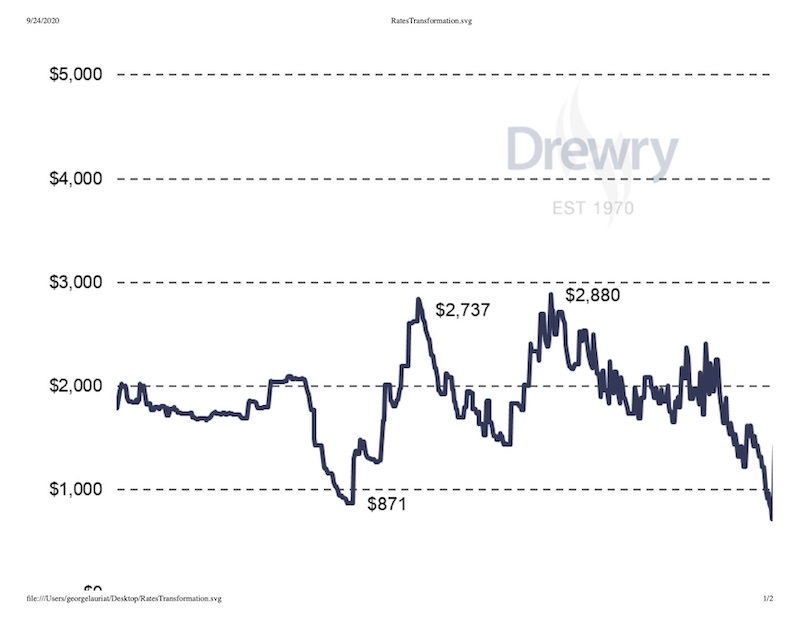

This week’s reading for the Drewry Hong Kong-Los Angeles spot freight rate benchmark ($/40ft container), the first spot rate index tracked in the container shipping industry, topped the previous record ($2,880 in 2012) by $1,201/40ft box, broke the $4,000 threshold and reached a 15-year high of $4,081 per 40ft container – more than double the long-term average price.

How is this possible? Where are the anticipated benefits of the economies of scale and efficiencies achieved by carriers over the past 15 years?

As an independent consultant, bid management expert and provider of market insight for many years, we believe what we are witnessing is something beyond the usual dynamics of market supply and demand at work. True, Asian container shipments to the US are currently very strong, shippers are replenishing their inventories, there is a shortage of empty boxes in China and some shipping capacity has been taken out by carriers through cancelled sailings. But the higher level of concentration in the ocean carrier industry, combined with new, tighter capacity management discipline among carriers are also behind these exceptional freight rate levels. Ocean carriers seem to have come to realise the opportunity presented by the COVID-19 crisis and that by managing capacity closely, they can manage prices with potency.

These developments will be concentrating the minds of shippers. Regulators in China and the US are already watching the market closely.

Because spot rates tend to be leading indicators of contract rates, contract shippers/Beneficial Cargo Owners should start to budget for higher contract rates on most routes in 2021.

With Asia-US West Coast spot rates currently at $4,000 vs 2020 contract rates typically closer to $1,500, is it possible that ocean carriers could set their 2021 contract rates at $2,000 or $2,500 or even $3,000 per 40ft container in their next tenders?

To address current market issues and procurement strategy changes, Drewry is supporting shippers/Beneficial Cargo Owners in several ways:

Shippers can get access to databases of spot rates on over 700 lanes;

Shippers can benchmark their contract rates against the Drewry Benchmarking Club rates of small, medium and large shippers;

Medium and small shippers can get access to lower contract rates or, with the support of Drewry’s bid management experts, secure better results by employing best practices and the latest bid technology;

Shippers can also obtain independent forecasts of contract freight rates on their specific routes (subject to having sufficient contract rate data and industry price driver data on the lanes concerned).