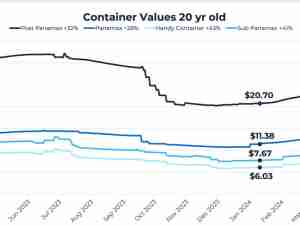

Key insights:

1 Easing demand and congestion saw China - US West Coast rates drop 25% last week, with the latest daily rates only 7% higher than in 2019.

2 Transatlantic rates, meanwhile, are down only 13% compared to last year and are nearly 3.5 times higher than in 2019, as demand for European imports has remained strong.

3 Chinese protests against covid restrictions are intensifying. Easing restrictions could ultimately result in more lockdowns, though with demand easing these disruptions would not be expected to have the same impact on logistics as they did earlier in the pandemic.

4 President Biden has asked Congress to pass legislation to resolve the dispute or push back the Dec. 9 strike deadline – and keep containers moving.

Ocean rates:

• Asia-US West Coast prices (FBX01 Weekly) dropped 25% to $1,935/FEU. This rate is 87% lower than the same time last year.

• Asia-US East Coast prices (FBX03 Weekly) fell 16% to $4,585/FEU, and are 73% lower than rates for this week last year.

• Asia-N. Europe prices (FBX11 Weekly) decreased 5% to $4,074/FEU, and are 72% lower than last year.

Analysis

Falling demand and easing congestion combined to push transpacific ocean rates down sharply last week, with the Asia - US West Coast weekly average declining by 25%.

Daily rates to the West Coast so far this week have dipped even further and are less than 7% higher than in November 2019, while East Coast prices which fell 16% last week still remain well above 2019 levels. Asia - N. Europe prices dipped 5% and remain 170% higher than in 2019. Ocean carriers are increasing the rate of blank sailings in December in the hopes of stabilizing rates.

Transatlantic rates, meanwhile, are down only 13% compared to last year and at more than $6,500/FEU are nearly 3.5 times higher than in 2019, as demand for European imports has remained strong and port congestion has helped to restrain some capacity.

But wildcards that could interrupt the overall trends of falling costs and easing delays remain.

Chinese protests against COVID restrictions are intensifying, including some high-profile disruptions to manufacturing. An easing of China’s “Zero COVID” policy could ultimately result in more lockdowns that could affect manufacturing and port operations. Though with demand easing and vessel capacity available, these disruptions would not be expected to have the same impact on logistics as they did earlier in the pandemic when demand was surging and capacity was already constrained.

The December 8th deadline to avoid a major rail union strike in the US is likewise approaching. And President Biden has asked Congress to pass legislation that would either compel the sides to accept the agreement brokered earlier in the year or push back the strike deadline to let negotiations continue – and keep containers moving.