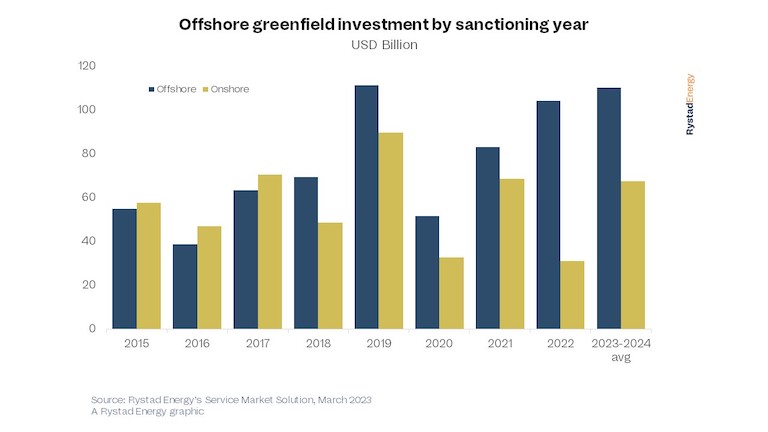

The offshore oil and gas (O&G) sector is set for the highest growth in a decade in the next two years, with $214 billion of new project investments lined up. Rystad Energy research shows that annual greenfield capital expenditure (capex) will break the $100 billion threshold in 2023 and in 2024 – the first breach for two straight years since 2012 and 2013.

As global fossil fuel demand remains strong and countries look for carbon-friendly production sources, offshore is back in the spotlight. Offshore activity is expected to account for 68% of all sanctioned conventional hydrocarbons in 2023 and 2024, up from 40% between 2015-2018. Comparisons against this period are prudent as it predates the Covid-19 pandemic and related oil price crash. In terms of total project count, offshore developments will make up almost half of all sanctioned projects in the next two years, up from just 29% from 2015-2018.

These new investments will be a boon for the offshore services market, with supply chain spending to grow 16% in 2023 and 2024 , a decade-high year-on-year increase of $21 billion. Offshore rigs, vessels, subsea and floating production storage and offloading (FPSO) activity are all set to flourish.

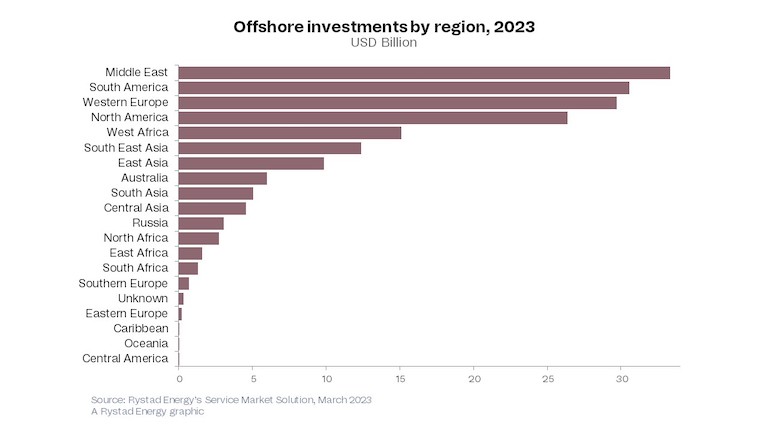

One of the leading global drivers is the sizable expansion of offshore activities in the Middle East. For the first time, offshore upstream spending in the region will surpass all others, lifted by mammoth projects in Saudi Arabia, Qatar and the UAE. The area’s offshore spending growth looks set to continue at least for the next three years, growing from $33 billion this year to $41 billion in 2025. These countries are tapping into their vast offshore resources to meet rising global oil demand, backed by the necessary capital and infrastructure to outpace other producers.

“Offshore oil and gas production isn’t going anywhere, and the sector matters now possibly more than ever. As one of the lower carbon-intensive methods of extracting hydrocarbons, offshore operators and service companies should expect a windfall in the coming years as global superpowers try to reduce their carbon footprint while advancing the energy transition,” says Audun Martinsen, head of supply chain research with Rystad Energy.

Although the Middle East is leading the way, South America, the UK and Brazil are just slightly behind. Investments in the North Sea from the UK and Norway will rise in the next two years. UK offshore spending is set to jump 30% this year to $7 billion, while Norwegian investments will hit $21.4 billion, an increase of 22% over 2022. Brazilian upstream spending is projected to approach $23 billion this year, with Guyana investments totaling $7 billion. In North America, spending on offshore in the US will top $17.5 billion and $7.3 billion in Mexico.

Brazil state giant Petrobras plans to deploy 16 FPSOs across six fields before the end of this decade, while growth in the Guyanese Stabroek Block will also contribute to regional expansion. In long-term forecasts, Middle Eastern growth is set to continue, if not accelerate, while South American spending will slow in 2025.