The following are the key takeaways from the main report published today, "The Energy Transition And COVID-19: A Pivotal Moment For Climate Policies And Energy Companies":

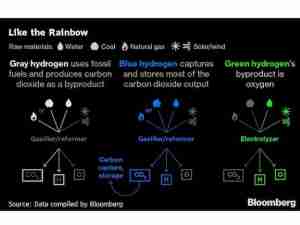

However, the pandemic's effects will cumulatively lower energy sector CO2 combustion emissions by 27.5 gigatons over 2020-2050--equivalent to almost one full year of emissions. To be sure, a mosaic of solutions beyond just renewables and fossil fuel demand destruction--such as hydrogen, carbon capture utilization and storage, and biofuels--will be needed. That decline is, however, not enough to substantively bring forward the year of peak oil demand that S&P Global Platts Analytics projects for the late 2030s. Under its sensitivity analysis, oil demand could peak in 2025 if policies and business and consumer behaviors change drastically, including near total adoption of working from home, reshoring of supply chains, widespread electrification of road transportation, and a halving of air traffic. As for gas, the downward revision in global energy demand makes it more exposed than other fuel sources because as a transition fuel, it is squeezed between the decline in primary energy demand, the increasing penetration of renewables, and the stickiness of coal demand--particularly in Asia. The increased cost competitiveness of renewables, rising overall power system costs (given past heavy subsidies), and concerns about budgets are all weighing on policymakers' appetites for further incentives and tax credits. In China, renewable projects will have to compete at grid-parity prices starting in 2021, though the pipeline of such grid-parity pilot projects remains supportive. To keep funding costs low, projects require long-term price visibility in terms of power price agreements or fixed-price auctions, both of which are less available. Another increasing need is the integration with storage, as the share of renewables in the power mix grows. This, together with the economic uncertainty COVID-19 brings, means that larger energy players, with strong balance sheets and vertical integration--with dispatchable generation and natural hedging through retail--may be better positioned to consolidate the industry. The oil majors could play a role given their size, gas, and power trading, downstream fuel retail operations, and offshore expertise. BP has indicated it expects to employ by 2025 as much as 20% of its capital in transition businesses, including low carbon. Nevertheless, we expect the energy transition for oil majors will be long and challenging.

_-_28de80_-_58820516bd428ab3fd376933932d068c43db9a4a_lqip.jpg)