Forecasted Market Values are quarterly forecasts for individual vessels provided until the end of their predicted economic life.

Overall

The US China trade war is still on, but how negative its impact will be on global economic growth and shipping remains to be seen. With the Brazilian mine accident and the current geopolitical events unfolding, it is likely that total ordering activity will be softer near term, representing a downside risk to the positive development of newbuilding prices. Following increased combined total ordering activity (bulker, tanker, container, gas) in the first half of 2018, the pace slowed down.

While the sentiment is positive and ship prices are seen moving upwards in the forecast, near term uncertainties are likely to have investors taking a more cautious stance on ordering. Though the total orderbook for vessels has picked up from its bottom in 2017, it is still at levels giving the shipyard industry cause for concern, leaving investors and shipowners with the upper hand in newbuilding price negotiations. Implementation of IMO 2020 is expected, through reduced speed and inefficiencies, to shave off supply capacity going forward.

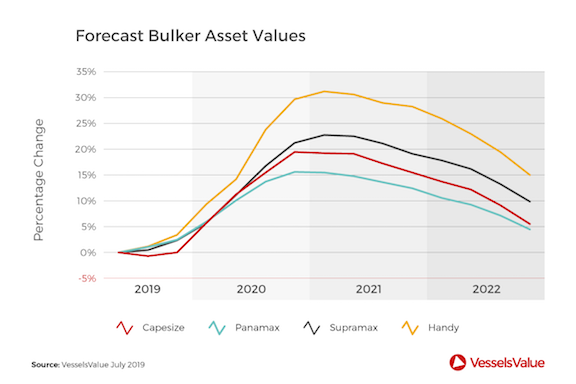

Dry Bulk

Demand, negatively impacted by the Brazilian mine accident, was outpaced by supply growth during the first quarter of 2019. The iron ore and coal development have put substantial upward pressure on dry bulk freight rates after declining dramatically during most of the first quarter. Capesize freight rates have more than quadrupled (from USD 3,500/day to USD 19,500/day), while other segments have increased moderately or remained flat through the second quarter.

Dry bulk demand growth should continue to be fueled by global economic growth, Chinese stimulated infrastructure investments, and seaborne trade of coal to China and Asia. Demand growth is expected to slow during 2021 and 2022 due to slower global economic growth.

Values marginally weakened during the second quarter after remaining flat during the first quarter.

Deliveries will increase as new vessels ordered during the mini boom of 2017/18 will enter the market during 2019 and 2020 with the dry bulk fleet still growing by an average of 3.3% over the next two years. Ordering is expected to remain low which should ensure more moderate fleet growth during 2021 and 2022.

Tankers

Vessel values have shown a positive development, though product tanker vessels have lagged behind the larger vessels. An asset value upside is present during our projection period for both newbuild and secondhand tanker vessels. At the same time, the ongoing trade war is still casting a shadow on the outlook for economic development. Now it seems that the trade war is most likely to intensify before easing, giving a potential sentiment boost in the second half of 2020, for which the timing of a resolve remains highly uncertain.

Forecasted ton mile demand growth coupled with slowing fleet growth, in turn helped by increased scrapping, will give improved earnings and values for tankers. An anticipation of lower ordering activity in 2019 caused by the current unstable geopolitical environment will aid the balance towards the end of the forecast, though the positive momentum may cool as softer demand sets its mark. The market direction during our forecast period will of course hinge on oil production developments in non OPEC (US) and OPEC countries, the ensuing oil price, and its impact on demand in oil hungry nations like China and India. Moreover, trading patterns continue to evolve, with the most apparent changes in the Atlantic (US) for crude and in the Far East for refined products.

For the tanker newbuild sector, improved charter earnings and a positive sentiment should ensure that asset values will continue upwards and accelerate towards the end of 2019.

Scrapping activity in the first quarter totaled 1.7m DWT, which is the lowest since the second quarter of 2017. Ordering activity climbed to 6m DWT in the first quarter of 2019 from 3m DWT in the fourth quarter of 2018.

Container

Container trade volumes on the main trade lanes (Asia to North America and Asia to Europe) showed a strong trend over the winter of 2018/19. The main reason for the stronger growth rates to North America has been the ongoing trade war with China, where shippers were fast forwarding goods ahead of an expected US tariff increase scheduled for March 1, 2019. Manufacturing has declined dramatically since the end of 2018 and industrial demand indicators are pointing towards even lower levels in the short term. Growth rates will be lower in the second half of 2019 and info the first half of 2020, before rebounding on expectations of a trade war solution. In Europe, both consumer confidence and industrial demand indicators are declining but imported volumes are growing so far. This positive trend will dampen towards the new year but rebound during 2020.