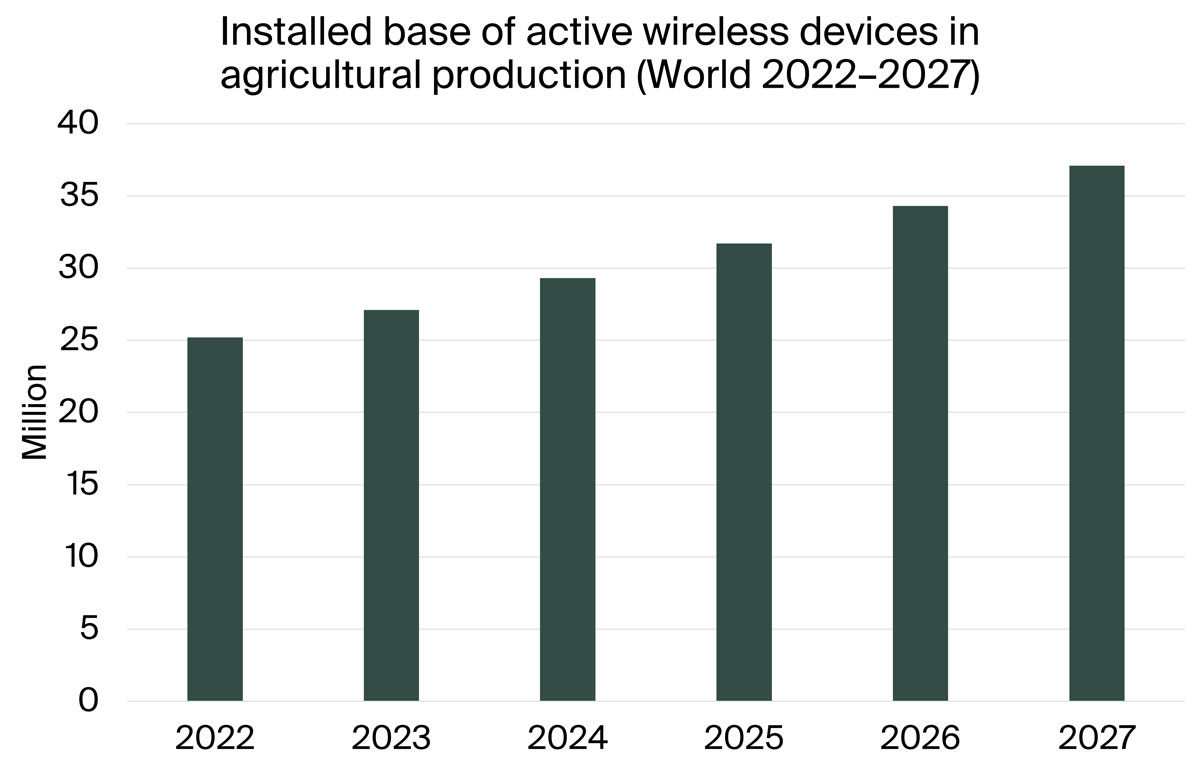

According to a new research report from the IoT analyst firm Berg Insight, the global market for precision agriculture solutions is forecasted to grow from € 3.1 billion in 2022 at a compound annual growth rate (CAGR) of 11.4 percent to reach about € 5.2 billion in 2027. A set of technologies are applied in precision farming practices, which are aimed at managing variations in the field to maximize yield, raise productivity, and reduce consumption of agricultural inputs. While solutions such as auto-guidance and machine monitoring and control via on-board displays today are mainstream technologies in the agricultural industry, telematics and Variable Rate Technology (VRT) are still in the early stages of adoption. Interoperability between solutions remains a challenge, although initiatives to provide common protocols and language structure for data sharing are making progress.

Most major agricultural equipment manufacturers have today operations related to precision agriculture with varying strategies. Leading vendors of precision agriculture solutions include the world’s largest manufacturer of agricultural equipment Deere & Company, followed by the precision technology vendors Trimble, Topcon Positioning Systems, Raven Industries, and Hexagon. Major input manufacturers like BASF, Bayer, Corteva Agriscience, and Syngenta have entered the space primarily through acquisitions and focus on providing mapping tools and decision support for the purpose of input optimization and yield maximization. A group of companies have surfaced as leaders on the nascent market for in-field sensor systems. These include Semios, Pessl Instruments with its METOS brand, Davis Instruments and Sencrop.

The move from automation to autonomy is the next step in the evolution of the agricultural industry. “Although autonomy on a component level has been exploited by multiple manufacturers, autonomous agricultural operations on an equipment level are now on the rise”, said Veronika Barta, IoT analyst at Berg Insight. Today, original equipment manufacturers are developing autonomous machines such as driverless tractors and seed-planting robots. Agricultural drones are the most advanced segment, performing autonomous operations by utilising multispectral cameras, LiDAR sensors and route algorithms. Aerial imagery for crop monitoring is the most common application area, followed by spraying operations of crop protection chemicals. Satellite navigation, sensors, artificial intelligence and machine learning will be the main facilitators of autonomous equipment in the future of farming.