Boston is a pattern of neighborhoods. The airport and port itself are all merged in close proximity, linked by a bewildering collage of streets and alleys that has made the local saying “you can’t get there from here” seem very real.

Boston is at once both small and large. The city roughly has a population of 670,000 but the greater Boston area is nearly 7.6 million. Perhaps more than most North American cities, Boston is a great deal more than permanent city-dwellers. Every year 350,000 plus undergrads take up residence accounting for $4.8 billion in economic activity.

From a metropolitan GDP perspective, Boston is the 6th largest in the U.S. and 12th largest in the world. In short, there is a remarkable amount of economic activity confined to a very small area, which brings up the port component of the City of Boston.

Northeast Ports

The Port of Boston has in recent history been measured more against what it is not, more than what it is. It is not the Port of New York/New Jersey mega-port handling 4.56 million TEU in 2016 (200 miles from Boston), nor a Port of Montreal at 1.34 million TEU (300 miles) or even the Port of Halifax (400 miles) – major ports which bracket the New England region. But what the Port of Boston is, or more properly has become, is very special. To understand what the Port is now, it is necessary to take a few steps back in time.

While the Port of Boston is not a mega-port in the same sense of the Port of New York/New Jersey, it is nevertheless the “Hub” for greater New England – an area including parts of upper-state New York and Canada south of the St. Lawrence River. This is not to say other ports like Portsmouth, NH; Portland, Maine; Davisville, Rhode Island and the Connecticut ports of New London, New Haven and Bridgeport, aren’t important to freight movement but rather the Port of Boston is the region’s principle container port – and is more than holding its own against competition throughout the East Coast. This wasn’t always the case. It was an uphill fight for market share. It was often remarked that New England’s real port was New York/New Jersey. Trucks shuttled boxes to and from New York/New Jersey, along with containerized barge services (services now gone – but the concept is still alive and under study).

The situation began to turn when Conley Terminal, the terminal facility closest to the sea, was designated as the port’s “container” operation.

By concentrating all the efforts on the one terminal – the terminal closest to the sea - the port’s prospects began to improve and a new vision began to emerge.

However, there were and are a number of obstacles to achieving the vision of a regional “hub” albeit niche port (see Michael Vanderbeek -The future of container shipping may be smaller than we think).

Back in June 2014, the then President Obama signed the Water Resources Reform and Development Act (WRRDA) into law and the Port of Boston’s $300 million plus Boston Harbor Dredging Project took an important step towards reality. Under the plan, the North Entrance Channel will deepen from 45 ft. to 51ft and the Main Channel from 40 ft. to 47 ft., along with two 50 ft. berths at Conley Terminal. Massport has received two significant funding sources with $107.5 million dollars in state funding to build a new berth and procure three larger cranes and another $42 million dollar Federal FASTLANE Grant to maintain and modernize the existing terminal. Overall, the potential port investment exceeds $800 million.

Cumulatively, these port infrastructure improvements remove the need for larger containerships to play the tides – thus leveling the playing field with other East Coast ports.

The Tide Turns

Historically, the main criticism with the Port of Boston (and many mid-sized) ports was that the productivity was low in comparison to larger ports. Some of these issues were a result of the nature of business. Smaller container vessels, with inherent imbalances in trade (at points in time as much as 70%-30% inbound to outbound) coupled with lower capacity equipment and a Northeast climate, made handling costs seem high vis-a-vis other Northeast container ports competing for the same business.

Once Massport made the commitment to Conley, the tide began to turn and the numbers started to climb. Consider in FY 2010, the port throughput was 173,735 TEU – not a bad year given the economic debacle of the Great Recession – but a mere six years later in FY 2016 the port throughput was a record 247,329 (2016-CY 248,391 TEU) outpacing average port growth in the East Coast, Gulf and Pacific. And there are no signs of the Port’s slowing down. To be sure, this is not a New York/New Jersey mega-figure, it represents something few in the industry thought would ever happen – a 200,000 plus TEU (actually three straight years) performance.

While some of the reasons for these increased throughput numbers is purely economic opportunity – there are plenty of well-heeled consumers just a stone’s throw from the terminal. For example, MSC (Mediterranean Shipping Company) arguably the largest (or second largest depending on measure) global containership operator has been calling in Boston for over 30 years, proof there is an economic draw. At least as important as the investment is the change in strategy emphasizing terminal productivity. The biggest caveat in the argument for “economies of scale” – the mantra for all containership operators, is productivity. Nearly all mega-metro ports like the Port of New York/New Jersey or LA/Long Beach, while having enormous advantages in scale of activity, have on and off-terminal productivity issues. Simply put, traffic congestion slows truck turns.

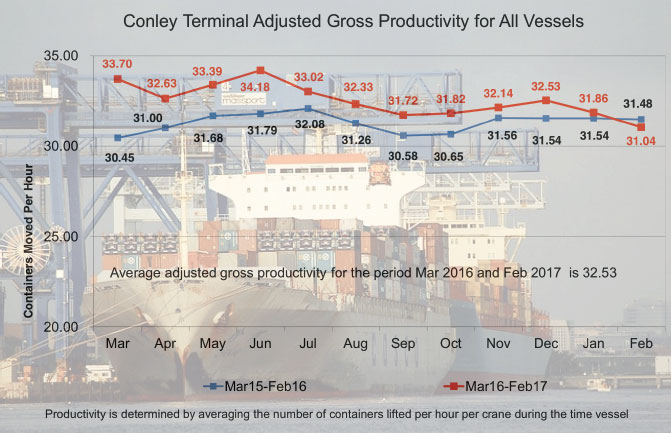

The longer time spent in lines going to the terminals or waiting in traffic, the lower the productivity in the bigger sense. In the Northeast case, it is difficult to turn trucks between Boston and the Port of NY/NJ in a day. In Conley’s case, the truck terminal turn-around time generally averages just over 32 minutes (see chart Mar. 16/Feb. 17) - a highly competitive turn time.

A second element of the emphasis on productivity is gantry cranes. Massport and the International Longshoremen’s Association (ILA) agreed to an innovative union contract based on crane productivity. The deal has produced results.

During the period Mar. 16-Feb. 17 (see chart) the lowest monthly average per crane lift/per hour was just over 31 in February 2017. This per crane productivity ranks very high, particularly considered with the weather, number of moves and size of vessels.

Without a shift in strategy and investment in the facilities and infrastructure (see above), it’s unlikely the Port of Boston would have grown or would be in the position to grow.

Future-Port

The Port of Boston is in line for another 200,000 plus TEU year in 2017. A number which begs the question of potential. Some boxship analysts believe that the port has the potential, without significant changes in the current footprint (the 100-acre terminal site has land immediate adjacent for expansion), to be a half million TEU port. Right now, the Port is on a statistical pace to be well over 400,000 before 2030. This estimate is probably low as it doesn’t take into account the changes in ship sizes and services.

Almost exactly a year ago, the Port of Boston handled its first 8,500 TEU vessel, an important test for the future of the port. Now virtually all the Asia trade vessels are 8,500-8900 TEU vessels and most calls are ships in excess of 6,000 TEUs.

The Port already has calls from the 2M (MSC/Maersk) and in April is adding new Asia services operated by the Ocean Alliance (CMA CGM, and its recently acquired American President Line (APL), Orient Overseas Container Line (OOCL), Evergreen and COSCO Shipping) and THE Alliance (Mitsui O.S.K. Lines, Nippon Yusen Kabushiki Kaisha (NYK Line) and Kawasaki Kisen Kaisha (“K” Line), Hapag-Lloyd, United Arab Shipping Company (UASC) and Yang Ming Transport. The three Japanese carriers plan on combining their container operations into one company by April 1, 2018. In addition, Hapag-Lloyd and UASC are to merge later in 2017.

The combination of alliance schedules gives the Port substantial reach, as well as calls that should boost throughput.

In the long term, dredging and improvement to the existing footprint remain the key to retaining and building services.