Corporations showing improved performance thanks to lower import levels

Three leading U.S. steel companies have reported enhanced profitability recently, in one case, less egregious negative results. All three attribute their brighter financial picture to falling steel imports and those thanks to the trade sanctions the United States government has imposed on foreign steel producers, most notably China, but others as well.

These results come at a time when a stronger U.S. dollar could have contributed to high levels of steel imports into the U.S. market, bolstering the argument that trade measures are starting to work to the benefit of the domestic industry. They also come on the heels of the American Iron and Steel Institute’s 2015 statistical report which showed steel imports near record levels. This year’s import picture is decidedly different.

These more favorable conditions have also brightened the financial picture of a large U.S. scrap dealer and recycler, which reported big gains in productivity in its recent quarter.

Steel Dynamics, Inc., one of the largest U.S. steel producers and metals recyclers, provided guidance recently on its second quarter 2016 earnings, which have not yet officially been released. The guidance projected earnings in the range of $0.53 to $0.57 per share, compared to first quarter 2016 earnings of $0.26 per share and 2015 second quarter earnings of $0.22 per share, a remarkable spike in profitability. Demand in the automotive sector was strong and the construction market continues to improve, the company’s report noted, while demand from the heavy equipment, agricultural, and energy remained slack.

Nucor Corporation, a Charlotte-based manufacturer of steel bars, beams, sheet, plate, piling, joists, girders, and cold finished steel, among other products, also announced guidance for its second quarter. Nucor expects second quarter results to be in the range of $0.65 to $0.70 per share, an increase compared to the second quarter 2015 earnings of $0.39 per share and the first quarter of 2016 earnings of $0.22 per share, another healthy spike in profits.

United States Steel Corporation, the New York-based integrated steel producer, reported a first quarter 2016 net loss of $340 million, or $2.32 per share. This was worse than its first quarter 2015 net loss of $75 million, or $0.52 per share, but much better than its fourth quarter 2015 loss of $1.1 billion, or $7.74 per share. Despite its losses, U.S. Steel projects earnings for 2016 in positive territory, near $400 million, provided current market conditions continue.

“During the first quarter 2016, positive changes in the flat roll steel supply environment resulted in significantly improved sequential consolidated operating earnings, which increased over 175 percent to $132 million,” said Mark D. Millett, the company’s president and CEO. “Flat roll steel import levels have declined and customer inventory levels are better matched with actual demand requirements, supporting higher domestic steel mill utilization.” Millett agreed with the Steel Dynamics assessment that the heavy equipment, agricultural, and energy markets remain weak, while the automotive sector continues strong and construction is in recovery mode.

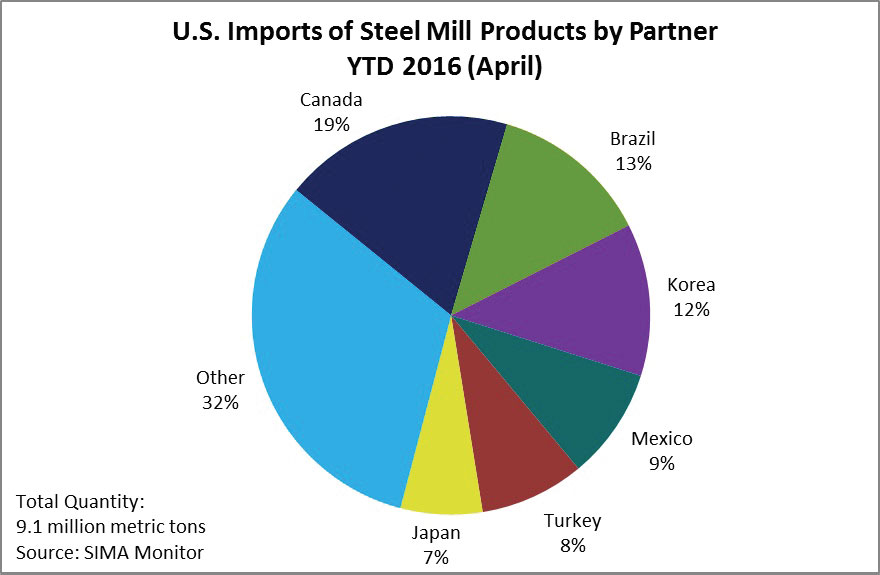

Statistics supplied by U.S. Steel indicate that imports of flat-rolled products are beginning to decline. Although import levels for rolled-steel products have fluctuated over the last year and half, the overall trend for imports of hot-rolled coil steel, cold-rolled coil steel, and galvanized steel has been down, and down dramatically since November 2014. Imports of hot-rolled coil steel in the month of November 2014, which were over 700,000 tons, sank in March 2016 to under 300,000 tons. Imports of cold-rolled coil steel—over 200,000 tons in November 2014—halved to around 100,000 tons in March 2016. Imports of galvanized steel dropped from 400,000 tons in November 2014 to 300,000 in March 2016.

“The decline is partially due to favorable trade case rulings,” said Millett, “but we are also seeing global prices rising, providing incentive for certain non-subject imports to stay in their home market rather than come to the U.S. Steel imports are down in the first four months of this year compared to the same period last year with preliminary duties in place and being collected.”

Trade Action Cases

The most significant improvement for Steel Dynamics was from the company’s flat roll operations, the company report noted. “Customer flat roll inventory levels are better aligned with steady consumption,” the report said. “As such, the reduction in imported flat roll steel due to trade case actions has resulted in supply-driven price appreciation.”

Domestic producers first launched cases before the U.S. Department of Commerce and the International Trade Commission in an effort to stem the increased flow of allegedly unfairly traded corrosion-resistant cold-rolled and hot-rolled steel products into the U.S. market in June 2015, that requesting anti-dumping and countervailing duties be imposed in the offending parties. Those proceedings resulted in countervailing duties of as high as 235.66% and anti-dumping duties of 255.8% on Chinese imports, and much lower sanctions against imports from the other markets in question.

In July 2015, U.S. steel companies filed a cold-rolled product case. The petitions charged that unfairly-traded imports of cold-rolled steel products from Brazil, China, India, Japan, South Korea, Netherlands, Russia, and the United Kingdom are causing material injury to the domestic industry. Those proceedings resulted in countervailing duties of as high as 227.29% and anti-dumping duties of 265.79% on Chinese imports, and lesser sanctions against imports from the other countries. Imports from Brazil were hit 7.42% countervailing duties and up 35.43% in anti-dumping duties, while the other countries received lesser penalties and the Netherlands was excluded from the case. In August 2015, six domestic steel producers filed petitions for the imposition of duties on hot-rolled coil imports from Australia, Brazil, Japan, South Korea, the Netherlands, Turkey, and the United Kingdom. Imports from the UK received anti-dumping duties of 49.05%, Australian imports were hit at a 23.25% rate, and sanctions on Brazilian products were as high as 34.28%.

Affirmative final determinations in the anti-dumping and countervailing duty cases of corrosion-resistant steel products were announced by the Department of Commerce in May. Final determinations in the three flat-rolled trade cases are expected within the next few months. “Our efforts to improve U.S. trade laws and their enforcement have started to be reflected in preliminary trade rulings,” said Millett. “This is a positive step toward establishing a fair market environment in the U.S., but we remain a long way from truly resolving the trade practices that are harming the domestic steel industry. While we will benefit from the improving market conditions, the global steel industry continues to face many challenges.”

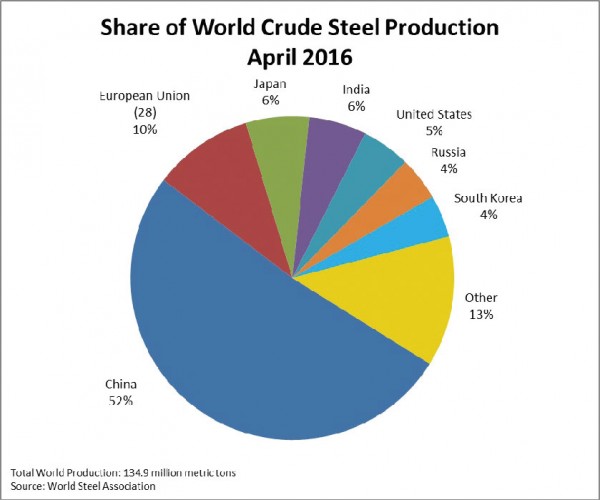

One such challenge is that the overcapacity in the global steel industry, and in China in particular, has yet to be addressed. If China chooses to ramp up its production once again, U.S. producers may still have to face downward pressure on global steel prices.

Peter Buxbaum has been writing about international trade and transportation, as well as security, defense, technology, and foreign policy, for over 20 years. Besides contributing to the AJOT, Buxbaum’s work has appeared in such leading publications as Fortune, Forbes, Chief Executive, Computerworld, and Jane’s Defence Weekly. He was educated at Columbia University.