In a merger between equals, the joining of Wilhelmsen & Wallenius Lines has created a market setting ro-ro powerhouse.WWL’s Tonsberg sails into Australia

In April, Wilh. Wilhelmsen ASA and Wallenius Lines created the world’s largest Ro/Ro-Pure Car Truck Carriers operator, with 78-vessels owned, another 39 on charter and six more now being built. The newly merged Wallenius Wilhemsen Logistics ASA, or WWL, also established a logistics powerhouse, with an impressive global presence in port, technical and inland services.

The structure of the transaction was noteworthy as well. This was a true combination of equals, unusual in the world of mergers and acquisitions. Wallenius was a private, family-owned company from Sweden. Wilhelmsen was from Norway and, while owned primarily by the Wilhelmsen family, was listed on the Oslo Exchange. Each of the two ended up with exactly the same ownership percentage of the merged entity: 37.8%. The remaining 24.4% is freely floated in the marketplace, shares having been sold down by Wallenius, to mostly institutional investors. The sale was substantially oversubscribed.

WWL is now listed on the Oslo Stock Exchange, where it is actively traded. Its market cap now tips $2.5 billion. Shares have increased 25% in value since its April debut, which technically took over the Wilhelmsen listing.

“It’s been very well received by the investment community,” said Andreas Wikborg, an Oslo-based shipping analyst with the brokerage firm Arctic Securities (Arctic Securities was one of the bookrunners on the sell-down of shares.)

That $2.5 billion market cap ranks WWL the eighth largest publicly traded liner logistics company in the world, although it’s still tiny compared to Danish liner A.P. Moller-Maersk, which is one of the biggest transport companies in the world, with a market cap of almost $40 billion.

Merger of Equals, Equals Partnership

According to Wikborg, the merger of equals was possible because the assets of the two companies were similar in size and age. And, the two companies were anything but strangers to each other. They had, in fact, established a joint venture partnership in 1999 that held joint ownership in three entities: the old Wallenius Wilhemsen Logistics, owned jointly 100%; EUKOR Car Carriers, owned jointly 80%; and American Roll-on Roll-off Carrier, owned 100%.

The biggest of these companies is EUKOR, which carries more than 4 million cars each year. The two acquired an 80% interest in Hyundai Merchant Marine Co.’s car carrier operation in August 2002 for $1.3 billion. Hyundai Motor Co. and Kia Motor Co. retained a 20% interest in EUKOR, which continues to ship mostly Korean cars.

WWL said the desire to merge, add assets each owned individually and keep ownership equal was “the next step” in their partnership.

“It was quite a unique situation,” said Wikborg.

This deal underscores a consolidation in the ownership of ro-ro/PCTC operations, in the face of auto manufacturers pushing hard to pare transport costs. That consolidation is far more advanced than what has taken place in either container or bulk lines.

“It’s not as fragmented as the rest of the industry,” said Wikborg.

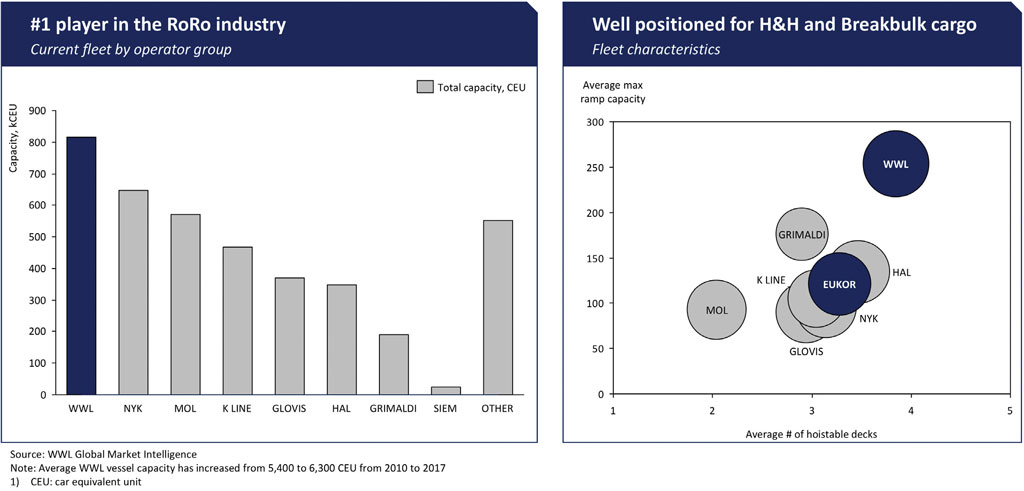

The above chart provided by WWL in its presentation to perspective investors tells the story: Within the world of ro-ro’s, WWL now controls about 20% of the global car equivalent unit or CEU capacity. Three Japanese players – NYK, MOL and K Line – each operate between 12% and 18%. Three more companies – Korea’s Hyundai Glovis, Norway’s Hoegh Autoliners and Italy’s Grimaldi – control between 5% and 10%. The remaining companies control less than 20%.

This doesn’t mean, however, that there’s less competition among carriers. Overcapacity dogs the ro-ro industry as well. (see sidebar on an analysis of the industry on page 21).

WWL entities chalked up almost $3 billion in ocean transportation-related revenue in 2016, with another $700 million in logistics services.

The WWL merger takes place amidst uncertainty in the global car business. In 2016, according to research conducted by Clarkson’s, seaborne car imports into the Middle East, Africa and South America declined by more than 10%, while North America grew by 2% and Europe by 4%. According to projections by IHS, global auto sales until 2021 will grow only about 1.8% annually, although deep-sea transport should increase about 2.1% a year. The US is projecting a fairly flat demand in the years ahead, while parts of Asia should continue to boom. China will likely emerge as a vehicle exporter of note over the next several years.

In an email exchange, WWL president and CEO Craig Jasienski addressed this changing landscape: “In mature markets, auto sales are expected to be relatively flat while the outlook for the emerging markets are mixed,” he wrote. “Overall, the expectations are slightly positive.”

After years of expansion, the US market is definitely slowing. This can create even more aggressive competition among the car carriers as well. “We see inventory levels for many manufacturers increasing and recognize that the US market growth will slow down,” wrote Jasienski, who was president and CEO of EUKOR Car Carriers before the merger. “We remain agile with our capacity and services and will adjust as and when we see volumes changing.”

China, on the other hand, Jasienski wrote, is a burgeoning focus of WWL. “Through our operating entities, we retain a strong interest with broad operations for vehicles in China, for imports, exports, land operations and short-sea services,” he said. “We work with Chinese and foreign makers to support their current and future finished logistics needs.”

Bigger Vessels

Major players are moving to bigger and bigger vessels and WWL is among those carriers leading the way. WWL now has four PCTC vessels with 8,000 CEU capacity each and six more that can carry more than 7,900 CEUs. The post-Panamax newbuilds will add to this bulk.

Jasienski said this type of build is the result of all sorts of factors, “With ever increasing cost of operating the business from Consumer Price Index related cost increases, to legislative changes and government determined tariffs, coupled with manufacturers demand for improved cost and quality, it is natural for the industry to seek economies through scale,” he wrote.

According to Wikborg, WWL “has a fleet size larger than its peers.” Its vessels average 6,600 CEUs, while the industry average is 5,500 CEUs. This larger size is critical not only because of the ability to carry more vehicles, but to carry larger and heavier project cargo. This is because of a higher deck space. According to WWL, the company’s biggest ships can handle project cargo up to 400 tons with dimensions six meters high, 50 meters long and 11 meters wide.

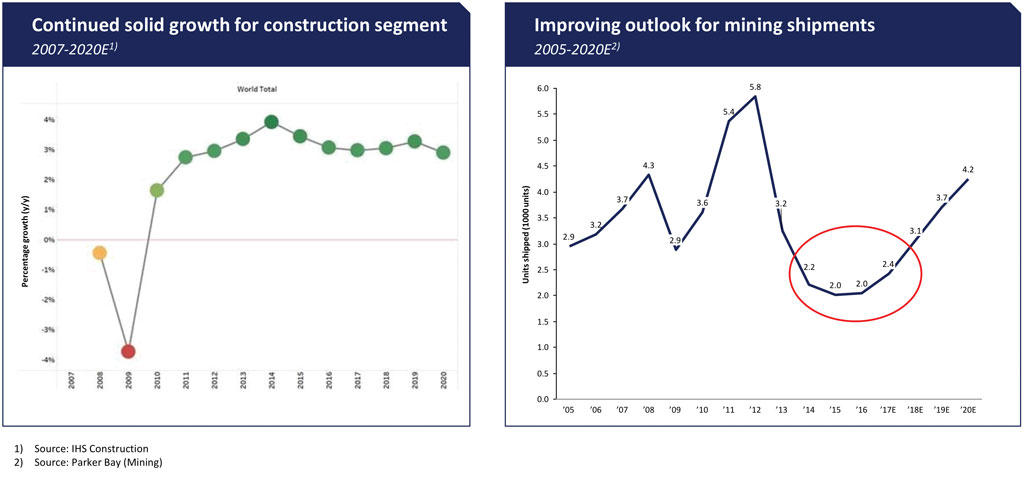

This “high and heavy” marketplace is an important part of ro/ro business with margins that are higher than shipping vehicles. Heavy equipment for construction, agriculture and mining has been depressed for some time, but it’s now forecast to grow, and in the case of mining equipment, substantially.

High and heavy shipments, plus some break bulk, constitute 22% of total cargo carried by volume on WWL ships. WWL believes its ability to carry this heavy cargo on scheduled routes are giving the carrier an edge over heavy lift vessels. It cites the recent transport of a mammoth industrial press used for the production of electric vehicles from Bremerhaven, Germany to Port Hueneme, California. The shipment, which other sources identified as bound for Tesla, was transported in three stages by three separate ships. One piece of equipment alone weighed 208 tons.

The company predicts that it can eventually save upwards of $100 million a year over the old entities through combining operations, back-office functions and better fleet optimization. Investors are banking on this as well.