Fitch Ratings has affirmed the 'AA' rating on $993 million in senior lien Port of Long Beach harbor revenue bonds and notes issued by the City of Long Beach, California. Fitch has also affirmed its 'AA-' rating on the outstanding but yet to be drawn $325 million subordinate TIFIA loan. The Rating Outlook on all bonds is Stable.

KEY RATING DRIVERS

The ratings reflect the port's strong market position, with resilient revenues from long-term contractual guarantees that are sufficient to cover both the port's outstanding senior debt obligations and the subordinate TIFIA loan when issued. Contractual guarantees should continue to provide revenue stability as the port proceeds with borrowing for its sizable $2.5 billion long-term capital improvement plan (fiscal 2018-2027 CIP). This plan, while costly, will help ensure the port's competitive position going forward. Maintenance of strong financial metrics and considerable liquidity in line with management's guidelines of 2.0x minimum debt service coverage ratio (DSCR) and 600 days cash on hand (DCOH) are expected throughout execution of the CIP in order to support the port's ratings. The one-notch differential on the TIFIA loan reflects its subordinate claim on revenues.

Strong Market Position- Revenue Risk (Volume): Stronger

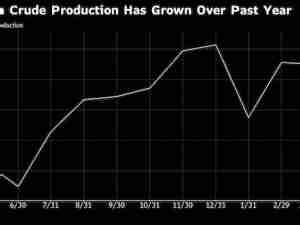

The Port of Long Beach is the nation's second largest container port, located on the west coast. Together with the neighboring Port of Los Angeles, it constitutes the San Pedro Bay Port Complex - the seventh largest port complex in the world. Fiscal 2017 20-foot equivalent units (TEUs) were 7.23 million, a 4.1% increase over 2016 that reflects recovery of volumes following the departure of two large shipping lines in 2016 (Hanjin due to bankruptcy and CMA CGM due to moving to Port of Los Angeles). The port's ability to handle larger ships, sizable local market share, and strong representation across the newest shipping alliances position the port favorably even as the shipping industry continues to see consolidation. Fitch also views port moves toward chassis management agreements as a positive development in alleviating port congestion.

Resilient Revenues Through Volatility- Revenue Risk (Price): Stronger

With a large majority of operating revenues coming from the container business (76% of operating revenues in fiscal 2017), the port is exposed to fluctuations in international trade and growing competitive pressures, which can lead to volume volatility. This has been especially true in 2016 and 2017 with the bankruptcy of Hanjin and the realignment of container shippers into new alliances resulting in volume fluctuations for Port of Long Beach and other ports worldwide. However, the port's revenues have proven to be largely insulated from trade-related revenue volatility due to the high percentage of long-term guaranteed contracts in place with most tenants. Fitch notes agreements have been honoured even through the Hanjin bankruptcy. Minimum guarantees accounted for 87% of operating revenues in fiscal 2017, and this share is expected to rise in the medium term as higher guarantees come online in connection with the completion of the Middle Harbor Redevelopment.

Modern Facilities, Sizable Capital Program - Infrastructure Development/Renewal: Midrange

While the port benefits from modern facilities, the port's capital program through 2027 is sizable at $2.5 billion, and funding for the program is expected to include an additional $645 million in borrowing in the next three to four years. The scope and cost of the CIP keeps the Infrastructure score at Midrange at present, though this may migrate upwards as large components of the CIP are completed. Careful management of the plan's scope and cost relative to business demand so as to maintain the port's strong financial profile is important to rating maintenance.

Fixed Rate, Amortizing Debt - Debt Structure (Sr): Stronger / Debt Structure (Sub): Midrange

Fitch views Port of Long Beach's Debt Structure as Stronger for the Senior Lien and Midrange for the Subordinate TIFIA loan. Senior bonds are all fixed rate and benefit from strong covenants, although Fitch notes future bonds are not structured to include a DSRF. The subordinate TIFIA loan is also fixed rate, and benefits from a fixed amortization profile, but has a junior claim to revenues. Fitch views positively the board's ordinance requiring maintenance of 2.0x DSCR (all-in) and 600 DCOH, which serve to protect bondholders as additional leverage for the CIP is brought online.

Financial Profile

The port has a healthy balance sheet with a strong liquidity position, even as cash is used for the ongoing CIP. Liquidity for 2017 of $408 million represents over 1,000 DCOH. Senior DSCR has remained near 3.0x since 2011, and rebounded to 2.7x in 2017 after dipping to 2.4x the last few years. DSCR is projected to remain at or above 2.1x in Fitch's rating case and downside scenarios. Port leverage for 2017 is low at 2.2x net debt/cash flow available for debt service (CFADS) on all obligations (includes TIFIA loan), though this is expected to rise to the 4.0x-5.0x range as borrowing for the full capital plan is executed over the next five years.

PEER GROUP

The Port of Los Angeles (AA/Stable) is the closest peer to Long Beach, sharing the San Pedro Bay and access to the Alameda Corridor. Long Beach's liquidity compares favorably to Los Angeles', and current metrics are comparable, while Long Beach's capital plan going forward is more substantial than that of Los Angeles and requires substantial additional borrowing over the next five years. Port Houston (IDR AA/Stable) is another comparable port, with access to tax revenues and comparable borrowing for its sizable CIP but lower guaranteed revenue.

RATING SENSITIVITIES

Future Developments That May, Individually or Collectively, Lead to Negative Rating Action:

- Higher than anticipated volatility or a steady downward trend in port container volumes;

- Financial forecasts indicating metrics falling below management's policy of maintaining 2.0x DSCR and liquidity equivalent to 600 DCOH; and

- Upward revisions to the capital program or debt funding that could indicate weaker debt metrics or measurably reduce port liquidity.

Future Developments That May, Individually or Collectively, Lead to Positive Rating Action:

- Given both the current rating level and the scope of the current capital plan, upward rating migration is not likely at this time.

CREDIT UPDATE

Performance Update

Port of Long Beach saw TEUs growth of 4.1% for fiscal 2017, buoyed by strong cargo performance during the second half of the year that offset declines seen in 2016 related to the bankruptcy of Hanjin Shipping. This recovery coincided with implementation of new alliance schedules calling the Port of Long Beach beginning in April 2017, including service strings by Mediterranean Shipping Company (MSC) calling at Total Terminals (TTI). TTI is the operator of Pier T Container Terminal, and was previously 54% owned by Hanjin. Under bankruptcy proceedings Hanjin sold its interest in TTI to a subsidiary of Mediterranean Shipping Company (MSC) and Hyundai Merchant Marine. Non-containerized tonnage also increased in the dry bulk category in fiscal 2017, due to a major contract being executed between a dry bulk tenant and a shipper. Despite these recent fluctuations, overall TEU growth remains in excess of GDP growth for the port, with the 2012-2017 CAGR at 4.3%. The first six months of fiscal 2018 have seen TEUs rise an additional 19%, with the sizable uplift reflecting the fact that the 1H2018 comparison period is the 6 months when neither Hanjin nor MSC was calling at TTI.

In fiscal 2017, the port's total operating revenues were $381 million, a 5.6% increase over 2016. The overall five-year CAGR for operating revenues shows an increase of 2.7%. Fiscal 2018 year to date through the second quarter has seen a further 13% increase in revenue due to the recovery of TTI from the Hanjin bankruptcy. Comparison of actual results to fiscal 2018 budget for the same period saw a 6% increase in revenue, due to a better than expected rebound at a major container terminal.

Fitch notes that declines and recoveries in volumes have had limited impact on the port's rating, largely due to the revenue stabilizing nature of the port's long-term leases with its largest tenants. These long-term lease contracts collectively contain minimum payment provisions that are more than sufficient to cover both the port's outstanding senior debt obligations and the future subordinate TIFIA loan, if drawn (covering all obligations at 2.1x on a net basis in 2017, and continuing to cover at 1.4x or higher through 2022). Even during periods of volume fluctuations (previously due to labor unrest and more recently due to carrier departures), minimum guarantees have been honored, and management indicates that key tenants desire to maintain long-term operations at the port. Contractual guarantees are expected to increase as the Middle Harbor project comes online (next sizable step-up expected in 2021). Guarantees will continue to provide revenue stability as the port proceeds with expected future borrowing for its sizable long-term CIP.

Historically, the port has maintained high DSCRs, with net coverage on all obligations in the 3.0x range both prior to the recession and since fiscal 2011. Coverage remains well above the rate covenant of 1.25x, at 2.7x in 2017. Cash reserves are extremely robust with $408 million in unrestricted funds, which translates to over 1,000 DCOH. The port manages to a minimum of 2.0x net coverage and 600 DCOH, per an ordinance adopted by the Board of Harbor Commissioners in October 2011. Fitch views this policy as providing liquidity stability for bondholders, and sees continued management to these levels as important to maintenance of credit quality as the port proceeds with borrowing for its capital program. Fitch notes that potential contingent liabilities to ACTA for debt payments are legally subordinate to port revenue bonds. Due to ACTA's restructuring of its debt, no additional ACTA shortfall advance payments are expected during the forecast period.

Fitch Cases

Both San Pedro Bay ports are well-positioned in terms of portside and inter-modal infrastructure, allowing them to accommodate local and non-local shipments. However, with up to 65% of cargo destined for inland markets, competition for this cargo may increase as ports on both the East and West Coasts compete for discretionary cargo volumes. Under various scenarios that contemplate drops in cargo volumes; funding of the full capital plan with an additional $645 million of debt obligations per management's projections; and careful management of operating and capital expenditures, forecasted DSCR for both senior and subordinate TIFIA obligations are expected to remain at or above 2.4x in a base case scenario, which assumes modest average annual revenue growth of 3.0% through 2022 and expense growth of 4.6% over the same period. In this scenario, leverage rises to 3.1x, reflecting expected additional debt for the CIP through 2021.

Fitch's rating case contemplates the blended effect over five years of a 10% drop in cargo coupled with 7% drop in revenues, followed by revenue recovery over a three year period. Over the five-year forecast period, this represents average annual revenue growth of 1.2%, coupled with expense growth of 4.6%. In this scenario, DSCRs for all obligations remain above 2.1x, and leverage reaches 4.3x by 2022 including CIP debt. Should volume stagnate or should the port fail to manage its expense profile prudently, the port may need to delay or defer certain elements of the capital program in order to maintain these coverage levels.

Failure to maintain coverage above 2.0x or liquidity above 600 DCOH in keeping with the port's debt ordinance will jeopardize the current rating.

Security

The senior lien bonds are secured by a pledge of and lien upon gross revenues. The Transportation Infrastructure Finance and Innovation Act (TIFIA) loan is secured by a lien on the port's subordinate revenues, or gross revenues remaining after the payment of debt service on senior bonds and the funding of any debt service reserve funds established for the senior bonds and any other senior obligations.