Key insights:

1 Salvage efforts are underway in Baltimore, with the Army Corp of Engineers estimating full water access to the port could be restored in weeks, not months.

2 Teams are first working to open a temporary channel for recovery vessels and some commercial traffic, though it will not accommodate larger vessels like container carriers.

3 Alternative East Coast ports are taking multiple steps – like extended gate hours, shifts of trucking capacity, and new rail service – to minimize the impact of rerouted volumes. Though shippers normally dependent on Baltimore will face higher costs and longer lead times, port officials in NY/NJ and Norfolk are confident they can handle additional volumes without disruptions.

4 So far, ocean rates to the East Coast have not increased and there are no reports of congestion.

5 Outside of the Baltimore impact, ocean rates may be reaching their new diversion-adjusted floor. Decreases from January/February peaks have slowed in recent weeks, and rate announcements suggest prices are approaching carriers’ hoped-for levels for April of $3k - $4,300/FEU to Europe/Med.

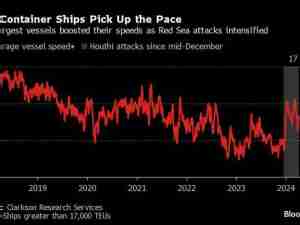

6 In air cargo, volumes out of China were strong in late March driven by B2C eCommerce, though FAX rates dipped to $4.23/kg to N. America and $3.31/kg to Europe this week. Red Sea diversions continued to increase air cargo demand out of S. Asia, with rates now at $5.25/kg to N. America, 75% higher than in mid-December, and $4.11/kg to Europe for a 129% increase.

Ocean rates - Freightos Baltic Index:

• Asia-US West Coast prices (FBX01 Weekly) fell 3% to $3,628/FEU.

• Asia-US East Coast prices (FBX03 Weekly) were level at $5,291/FEU.

• Asia-N. Europe prices (FBX11 Weekly) increased 2% to $3,258/FEU.

• Asia-Mediterranean prices (FBX13 Weekly) increased 17% to $5,307/FEU.

Air rates - Freightos Air index

• China - N. America weekly prices fell 25% to $4.23/kg

• China - N. Europe weekly prices fell 6% to $3.31/kg.

• N. Europe - N. America weekly prices fell 2% to $2.01/kg.

Analysis

Salvage crews have already started working to clear the wreckage from last week’s bridge collapse in Baltimore. Despite this task’s complexity and obstacles in the way, the US Army Corp of Engineers estimates it will take weeks, not months, to restore full access to the port.

Teams will first work to open a temporary channel allowing easier access for recovery vessels and restoring some commercial traffic to the port, though the dimensions and depth will not accommodate large vessels like container carriers.

Baltimore is the largest US port for vehicle imports and exports. Though many are anticipating disruptions and congestion in roll-on/roll-off operations, automotive leaders are saying alternatives are already in place and that they do not expect a significant impact to their operations.

In the container market, shippers who normally rely on the Port of Baltimore are being offered contingency plans from carriers to reroute volumes through alternative ports like New York/New Jersey and Norfolk. Expanded gate hours, additional trucking capacity – including from Maryland-area truckers – and an anticipated special New York - Baltimore rail service, are being put into place at these ports to accommodate the diverted volumes. Chassis providers are likewise confident there is enough supply to service the rerouting and warehouse and drayage providers are also rushing to adjust.

With these shifts and farther road/rail distances required, though, these shippers will face longer lead times and additional costs which will be a particular challenge for exporters of lower-valued goods.

In terms of any broader impact on container trade, Baltimore-bound vessels that add port calls at alternative ports will create some additional traffic there, while many that already make scheduled calls at these ports will need to offload more volumes during these calls.

But Baltimore is not a major player in regional or national container traffic, and with the above steps also aimed at minimizing any broader impact on container operations, port officials in NY/NJ and Norfolk, where some Baltimore volumes have already started to arrive, are confident that they will be able to handle the additional containers without disruptions. Indeed, so far, there are no reports of congestion at these ports and ocean rates remained level as well.

Outside of the Baltimore impact, ocean rates that had climbed sharply at the beginning of the year on Red Sea diversions and Lunar New Year demand may be reaching their new diversion-adjusted floor. Decreases from January/February peaks on the impacted ex-Asia lanes have slowed in recent weeks, and recent rate announcements by some carriers suggest they are hoping to keep rates at the $3,000 - $3,500/FEU level to Europe and $3,500 - $4,300/FEU level to the Mediterranean this month.

In air cargo, volumes out of China were strong in late March driven by B2C eCommerce growth, though Freightos Air Index China export rates dipped somewhat to $4.23/kg to N. America and $3.31/kg to Europe this week. Red Sea diversions continued to push some ocean demand to air out of S. Asia in March, where rates hit $5.25/kg to N. America last week, 75% higher than in mid-December, and $4.11/kg to Europe for a 129% increase.