SEA-LNG, the multi-sector industry coalition established to demonstrate the benefits of the LNG fuel pathway for shipping decarbonisation, has released a framework for comparing the emissions and cost implications of adopting future fuel pathways and urges the industry to make like-for-like comparisons when discussing alternative marine fuels.

The industry is making investment decisions now on new builds that will impact greenhouse gas emissions today and for the next 25-30 years, the typical lifetime of a vessel. It is essential the assessments of alternative marine fuel pathways are made on a like-for-like, or “apples with apples”, basis. Discussion of alternative fuels too often compares the green versions of ammonia and methanol with fossil, or grey, LNG. These green versions of ammonia and methanol are still some years away from commercial readiness, and should rightly be compared with green versions of methane, such as bioLNG or e-LNG (also known as renewable synthetic LNG).

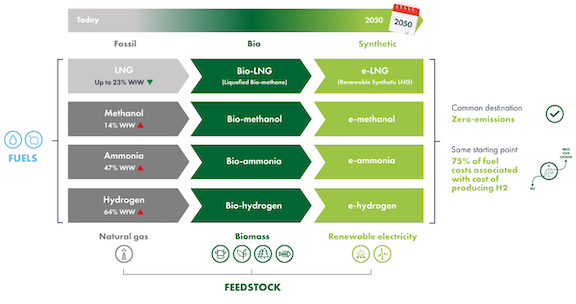

All alternative fuels share a common pathway, starting at fossil-based versions and ending at low and zero-emission hydrogen-based, synthetic fuels. These synthetic fuels will only become widely available when sufficient renewable electricity and electrolysis capacity comes online to produce them.

Adoption of zero-emission renewable fuels will not occur in a “big bang”. It is much more likely to take place incrementally as fuels are gradually decarbonised by blending with increasing amounts of low and zero-emission drop-ins.

Almost all alternative fuels today, including LNG, are fossil-based. In fact, most are produced from natural gas. LNG is simply natural gas that has been cooled to the point it liquefies. Natural gas, and sometimes coal, is also the feedstock for almost all methanol, ammonia and hydrogen production. While LNG offers significant greenhouse gas emissions reduction when used as a marine fuel compared with VLSFO, fossil methanol, ammonia and liquid hydrogen have far higher emissions on a well-to-wake basis. This will delay their adoption until a synthetic or biogenic version is available.

Committing to solutions which rely on alternative fuels that will not be available at commercial scale in a renewable form for the foreseeable future, means owners locking in higher-emission and higher-cost decarbonisation pathways. LNG as a marine fuel delivers immediate GHG benefits and a lower risk, lower cost, incremental pathway to zero emissions.

Steve Esau, Chief Operating Officer, SEA-LNG commented: “When looking at the advantages and disadvantages of alternative fuels, we should be assessing the characteristics of each fuel type on a like-for-like basis. Greenhouse gases in the atmosphere are a stock problem as well as a flow problem. The industry needs to consider the pathway to decarbonisation, not just the destination.

“There are consequences to delaying the shift from fuel oils, which will cause faster rising cumulative emissions. Shipping needs to assess fuel pathways based on how they can deliver decarbonisation benefits now, and in the future, and also the likely cost of these pathways”.