The Covid-19 pandemic has marked the end of an era for Southeast Asia’s combined oil and gas production, pushing the region’s output in 2021 to below 5 million barrels of oil equivalent per day (boepd) for the first time since 1998, a threshold that is not likely to be exceeded again in the future despite new project start-ups in coming years, a Rystad Energy analysis shows.

Daily average hydrocarbon production tumbled to 4.86 million boepd in 2021, down from 5.06 million boepd in 2020, and a massive 12% drop compared to the pre-pandemic volumes of 5.5 million boepd in 2019, Rystad Energy data shows.

Operators have struggled to regain production losses triggered by the pandemic as operators slowed down activity levels amid an unprecedented disruption in oil markets. The decline is projected to continue into the middle of the decade. Although volumes will remain stable in 2022, production will drop an additional 10% by 2025 to around 4.3 million boepd versus current levels.

“Liquids production in Southeast Asia has been on the decline for almost 20 years due to a lack of discoveries and project sanctioning activities in the region. While new government incentives may help, the region looks set to experience declining production levels well into the future,” says Prateek Pandey, upstream vice president with Rystad Energy.

By contrast, natural gas production in the region stayed steady between 2009 and 2019, at around 20.8 billion cubic feet per day (Bcfd). Despite expectations of a rise in gas sales volume that would counter the 8% fall in production in 2020, volumes are expected to be down around 2% this year compared to 2020, at about 19 Bcfd. This is primarily due to falling production at mature legacy projects including Mahakam, MLNG Dua and MLNG Satu PSCs, Yetagun.

The share of volume from projects under development and existing commercial discoveries are substantial and reflect the region’s timely execution of projects. Several projects were successfully brought onstream in 2021, including the highly anticipated Rotan field, utilizing PFLNG Dua, which started in March, making Petronas the only operator globally to produce LNG from two floating facilities. In Indonesia, Eni completed a timely development, with Merakes achieving its first gas production in April 2021.

However, despite these successes, Southeast Asia is still plagued by delays and stalled projects. In Indonesia, a recovery in gas production has been further delayed after the two significant developments -Tangguh LNG T3 and Jambaran Tiung-Biru Unitisation (JTB) - were postponed until 2022.

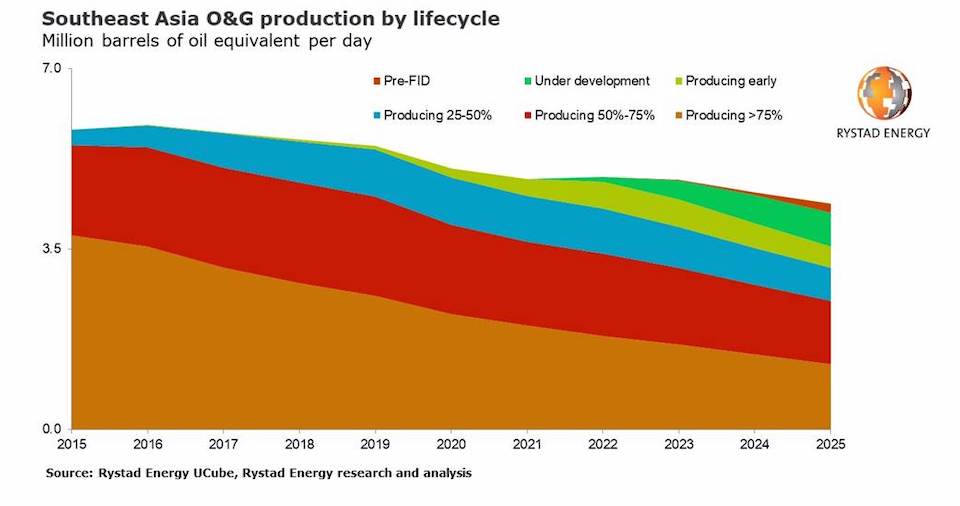

What the future holds

For most of Southeast Asia, over 60% of output comes from mature blocks – fields producing more than 50% of its resource. Volumes from such blocks are likely to see a consistent decline over the next few years, with an estimated 60% of production by 2030 likely coming from projects currently at the pre-FID (final investment decision) stage. Consequently, the driving force behind the region’s upstream outlook will be the sanctioning of new developments.

2020 was a nightmare year for regional sanctioning activity, with only around 300 million barrels of oil equivalent (boe) of resources from six assets reaching FIDs. As operators tried to move forward in 2021, the region has seen more than ten projects secure FIDs, with around 750 million boe of reserves and some $3 billion in greenfield investment, with Malaysia accounting for 85% of the total.

Sanctioning activities in 2022 are likely to remain at similar levels, with FIDs planned on around 800 million boe of resources in the region, of which 60% are in Indonesia and over 35% in Malaysia. Projects operated by majors and NOCs are likely to dominate in Malaysia, whereas regional players and E&P companies will primarily drive Indonesian developments.

However, planned FID projects in 2022 may still face challenges in securing the final approval. Indonesia’s domestic gas price regulation remains a concern for most large gas developments in the pipeline. Although incentives are being discussed for blocks such as Kasuri, it is still one of the factors that could further delay progress. The planned developments from production sharing contracts (PSC) due for current contract expiry in the near term are also at risk unless host country governments initiate early discussions on potential extensions.

Southeast Asia is unlikely to see a substantial increase in spending in 2022, with investments projected to be in the range of $15 billion to $20 billion across the year. Investments will likely be driven by increased drilling activity in mature blocks in Indonesia and Thailand, as NOCs take the reins and focus on top-producing blocks.

Around 360 million boe in resources have been discovered at eight fields as of November 2021, surpassing 2020 volumes by 40%. About 78% of total discovered resources this year in Southeast Asia are gas or gas condensate, while the remainder is oil. About 84% come from shallow waters, with around 86% at NOC-operated blocks. In line with the trend, over 90% of volume in the region in 2021 has been discovered in the Miocene-Clastic formation.