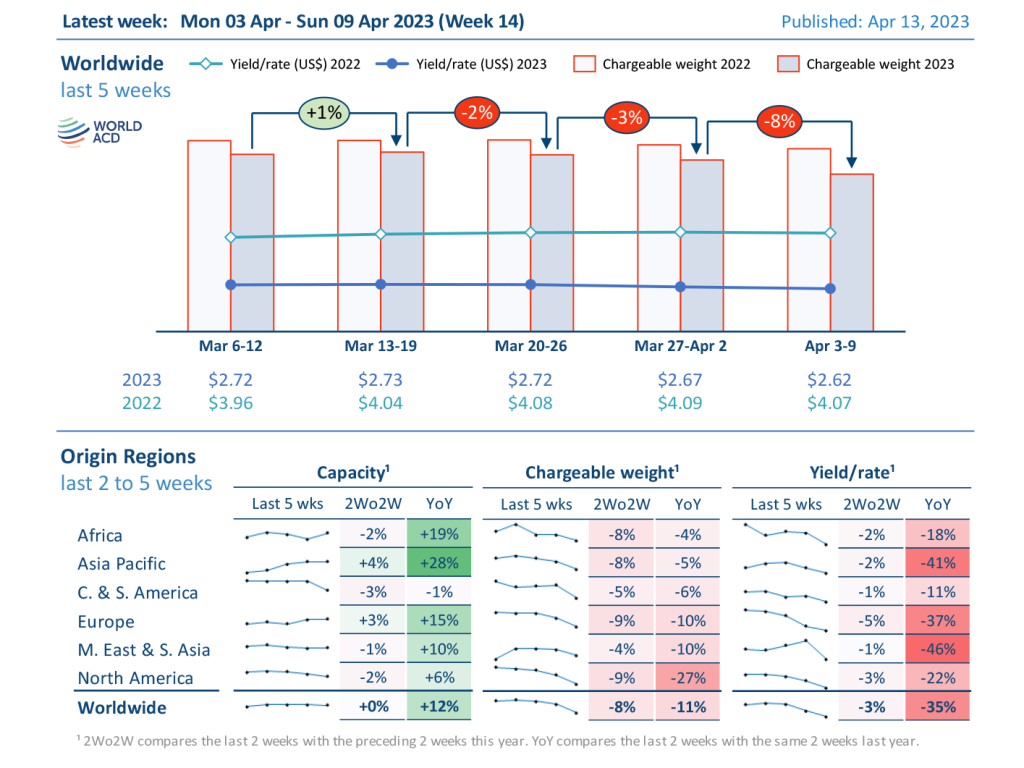

Worldwide air cargo demand has slipped further into decline after showing tentative signs of stabilizing in the last two months, with the first full week of April showing the steepest week-on-week drop since the Lunar New Year factory closures in January, preliminary figures from WorldACD Market Data indicate.

Following small week-on-week declines in weeks 12 (-2%) and 13 (-3%), last week saw a fall of -8% in worldwide flown tonnages, plus a further slight (-3%) drop in average global air cargo pricing – based on the more than 400,000 weekly transactions covered by WorldACD’s data.

Comparing weeks 13 and 14 with the preceding two weeks (2Wo2W), overall tonnages decreased by -8% versus their combined total in weeks 11 and 12, and average worldwide rates decreased by -3%, with capacity more or less stable.

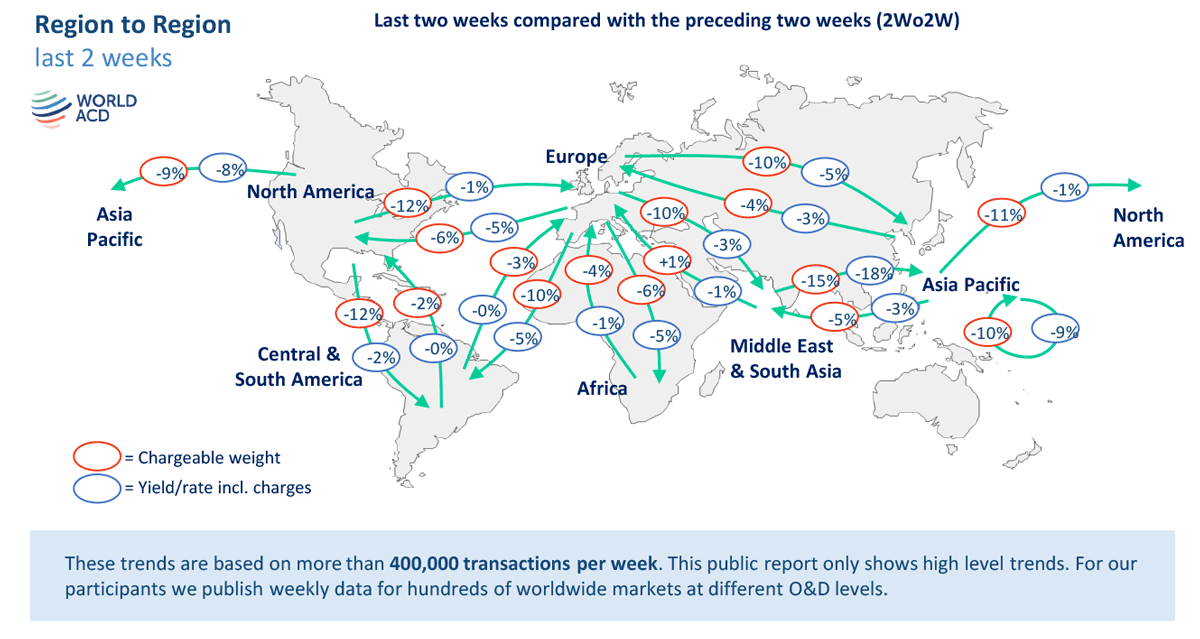

At a regional level, the downward trend in air cargo tonnages is visible from all of the main origin regions and on almost all lanes, on a 2Wo2W basis, particularly flows ex-Middle East & South Asia to Asia Pacific (-15%), ex-North America to Europe and to Central & South America (-12%), and flows ex-Europe to Asia Pacific, Central & South America and to Middle East & South Asia (-10%). Demand on the big lanes from Asia Pacific to North America and Europe also showed a significant decline (-11% and -5%, respectively), with only one regional lane showing a slight increase: Middle East & South Asia to Europe (+1%).

In terms of pricing, on a 2Wo2W basis, average yields continue to show a stable trend ex-Central & South America, but for all other regions average rates are decreasing, with the most significant drop seen from the Middle East & South Asia to Asia Pacific (-18%).

Year-on-Year perspective

Comparing the overall global market with this time last year, chargeable weight in weeks 13 and 14 was down -11% compared with the equivalent period last year – a return (after March’s -8%) to the double-digit percentage declines seen in the preceding five months. The notable percentage decreases in tonnages year-on-year were ex-North America (-27%), ex-Europe (-10%), ex-Middle East & South Asia (-10%). Also ex-Asia Pacific the trend compared to last year was negative (-6%), despite recent relatively positive developments from that region.

Overall capacity has jumped by +12% compared with the previous year, with double-digit percentage increases from almost all regions – except from Central & South America, which was slightly down (-1%), and North America (+6%). Most-notable increases were ex-Asia Pacific (+28%), ex-Africa (+19%), and ex-Europe (+15%).

Worldwide rates are currently -36% below their levels this time last year, at an average of US$2.62 per kilo in week 14, despite the effects of higher fuel surcharges, although they remain significantly above pre-Covid levels.