Despite a gloomy present, growing demand from India, Europe, automotive, and construction industries are expected to redeem the industry.

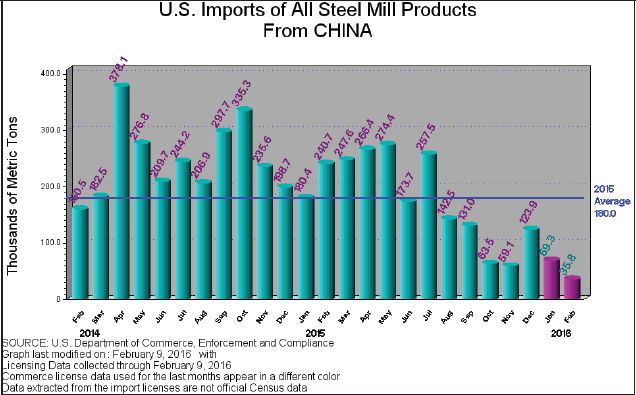

The steel industry experienced more disturbance in 2015 than in any year since the depth of the global financial crisis last decade. Looming large amidst the industry’s difficulties is China. The economic slowdown in China has dampened demand for steel and an oversupply of the metal has led to allegations of unfair trading practices by the world’s second largest economy. Falling oil prices and the consequent decrease in investments in that sector have also taken their toll.

For the industry in the United States, trade figures testify to the stark reality. Both exports from and imports of steel into the U.S. fell markedly in 2015.

According to the World Steel Association, global steel production decreased 2.8 percent last year and production shrank across all global regions. China’s production declined by 2.2 percent last year and its steel usage is expected to dip two percent this year. Meanwhile, China’s currency devaluations—which makes Chinese exports cheaper in foreign markets—has accelerated steel exports from China into markets with declining demand and has spurred allegation of unfair trading practices.

The steel industry’s exposure to the energy sector has also pulled down steel prices. The glut of oil will likely worsen as new Iranian oil comes on the market after the lifting of sanctions. “Steel demand from energy companies is expected to go down on declining capital expenditure budgets,” said an analysis from Zacks, an investments research firm. But Zacks also concluded that the automotive and construction industries, a growing economy in India, and an economic recovery in Europe give steel hope for the future.

U.S. steel exports fell by 17.2 percent from 2014 to 2015 to a total of 9.97 million net tons, according to figures released by the American Institute for International Steel. “A recession in Canada and a strong U.S. dollar contributed to a decrease in steel exports of more than one-sixth in 2015,” said Richard Chriss, executive director of AIIS.

About half of U.S. steel exports go to Canada. The amount of steel being sent north of the border fell by 23.3 percent to 4.9 million tons last year. This decrease of 1.5 million tons accounted for 75 percent of the overall export decline. Most of the remaining

decrease resulted from an 8.1-percent decline in exports to Mexico, which totaled 3.83 million tons in 2015. Exports to the European Union slipped two percent last year to 327,911 tons.

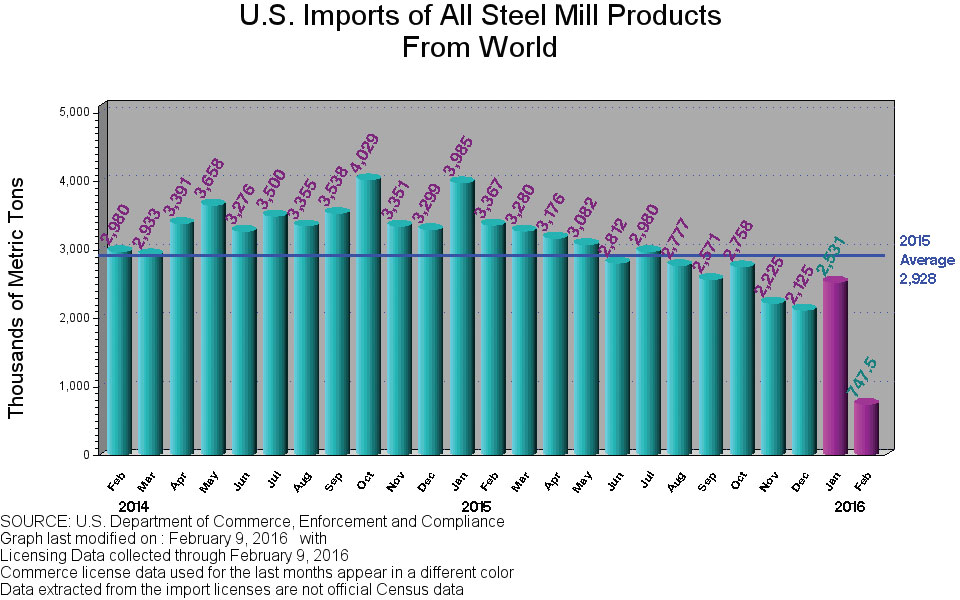

“The year ended on a slight up-note,” said Chriss, “as monthly exports increased in December.” The 1.9-percent increase from November was driven by a 10.2-percent growth of exports to Mexico, but that figure was still 12.5 percent less than in December 2014. Exports to Canada fell 4.2 percent in December. Steel imports closed out 2015 well below their 2014 levels, with the U.S. bringing in one-eighth less steel than it did the year before. Imports fell 12.6 percent to 38.77 million tons with the biggest decrease registered being in imports of steel from Russia, which was down 54.8 percent to 2.12 million tons. Imports from the European Union declined 15.2 percent, from Canada 4.2 percent, and from South Korea 11.4 percent.

“2016 may be a better year for exports, with moderate economic growth forecast for Canada and a stronger expansion expected in Mexico,” said Chriss. “Even if demand increases, though, the exchange rate is making American steel much more expensive abroad than it was even a year ago. Steel imports will likely continue to trend downward in 2016.”

The World Steel Association expects global steel use to grow a mere 0.7 percent in 2016 to 1.5 billion tons. That, combined with the strong dollar, the Chinese economic slowdown, and currency devaluations means that the U.S. steel industry continues to be under the threat of cheaper imports.

A number of countries, including the U.S., have initiated anti-dumping investigations against Chinese steel exports. In December, the U.S. Department of Commerce announced preliminary determinations in a countervailing duty investigations of imports of certain cold-rolled steel flat products from China. The petitioners in that case were AK Steel Corporation, ArcelorMittal USA LLC, Nucor Corporation, Steel Dynamics, Inc., and United States Steel Corporation.

The Commerce investigation determined that three Chinese exporters received subsidy rates of 227.29 percent. As a result, Commerce instructed U.S. Customs and Border Protection to require cash deposits on the Chinese imports at issue based on these preliminary rates.

Commerce also found critical circumstances to exist for the three subsidized Chinese exporters. That means that CBP will be instructed to impose provisional measures retroactively on entries of certain cold-rolled steel flat products. Commerce is scheduled to announce its final determinations in May.

The European Commission has also opened antidumping investigations to determine whether Chinese imports of three steel products have been dumped on the EU market. The European Steel Association (EUROFER) has repeatedly accused the Chinese government of interfering in the Chinese steel sector, because it wants to boost the Chinese exports at the expense of the rest of the steel industries around the world.

Axel Eggert, director general of EUROFER, said that volumes of dumped steel imports from China have doubled in the last 18 months. “They are flooding the EU market and directly causing irreversible closures and job losses across the EU steel sector,” he added. “China has domestic steel overcapacity of around 400 million tons, almost three times the total EU steel demand of 155 million tons. This overcapacity has arisen as a result of persistent state intervention in the Chinese economy.”

Despite the gloomy present, the Zacks report sees some light at the end of the tunnel for the global steel picture. India is expected to act as the next growth engine and the European economy is on a slow road to recovery, with steel demand expected to increase by 2.2 percent this year.

“Although the steel industry will remain under pressure for some time,” the report concluded, “it is certainly expected to grow thereafter, riding on the back of automotive and construction industries.”

Peter Buxbaum has been writing about international trade and transportation, as well as security, defense, technology, and foreign policy, for over 20 years. Besides contributing to the AJOT, Buxbaum’s work has appeared in such leading publications as Fortune, Forbes, Chief Executive, Computerworld, and Jane’s Defence Weekly. He was educated at Columbia University.