“Late February, and the air’s so balmy snowdrops and crocuses might be fooled into early blooming. Then, the inevitable blizzard will come, blighting our harbingers of spring…” Gail Mazur, The Idea of Florida During a Winter ThawBloom or Dust.

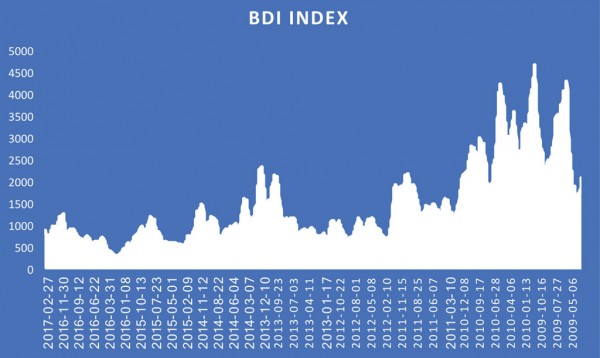

Just a little over a year ago, February 10th 2016 to be exact; the BDI (Baltic Dry Index) fell to 290 points, a historic low for the index, which measures dry cargo shipping activity. Now, the BDI is emerging from the gloom and as of this writing [March 2nd 2017] has cracked the 900 level, putting the index up over 164% for a 52-week period. Although this rise in the BDI is a significant indicator of an improvement in trading conditions, it is worth remembering that back in 2008 the index peaked at 11,793, just before the collapse with the onslaught of the Great Recession. During the following two-and-half weeks, the BDI shed nearly 94% of its value and never fully recovered. The moral of the story: what goes up often comes down a lot quicker. Using the 2008 BDI peak might be an unfair point of comparison – after all from the inception of the “new” Baltic index system in 1985, until the first real spikes in 2003, the BDI generally bounced between 1500-to-2000. However, since 2002 until 2012, the BDI has been in a bloom and mostly dust cycle, - few very profitable springs followed by the entire market biting the dust. (see charts on page 6 and 15)

From a technical stand point, the BDI is an evaluation of the price (or costs) to ship raw material – essentially commodities – around fifty well established shipping routes by ship size.

The larger ships tend to move major bulks like ores – especially steel making related products – while the ships on the smaller side move a wide range of minor bulks (see Matt Miller’s cocoa story on page 8) or piecemeal shipments. Often neo-bulks move either by breakbulk ships or unitized container or ro/ro vessels, with unitized freight rates often undercutting breakbulk.

From a larger frame of reference, there is a strong bond between the BDI and global economic health and well-being. The seaborne movement of essential commodities to economic growth, such as steel making products, makes the BDI a bellwether to future economic activity - albeit more as a comment in hindsight, than as a glimpse into a certain future. The world GDP has been in slowdown since 2010. GDP growth has decreased from 5.4% in 2010 to about 3.4% in 2014, 3.1% in 2015 and latest estimates have 2016 at 3.535%. Not impressive, but encouraging.

The oft quoted BDI link to GDP works in both directions. GDP forecasts often take BDI into account while BDI forecasts take GDP forecasts into account. It’s incestuous accounting and depends a great deal on the accuracy of the reports.

For example, one of the charts most often used to show the correlation of BDI to GDP growth is China. China is the greatest source of bulk shipments and thus has the biggest impact on movements. From 2000 until late 2007, with only minor exceptions, the BDI grew slower than China’s GDP. For the immediate time after the Great Recession, the BDI – even in freefall – outperformed China’s GDP. Since mid-2009, the GDP in China is again growing faster than BDI and the gap is running at a relatively stable pace, two indices moving in lock step. In a bit of revisionist history, was China’s GDP really growing at the 8%-13.5% or perhaps moving at a lower clip closer to the BDI? Since supply & demand involves a human element, would the anticipation of a rising China market influence investment and the bulkship orderbook and cause an over-supply of ships?

Inelastic Supply

In some respects the dry bulk market represents one of the purest examples of supply and demand economics. In the simplest terms, the transaction is cargo space in the ships versus the demand for that space from sellers of the freight (commodities). Presumably, the freight satisfies the demand in the buyers’ home-marketplace.

But matching supply and demand is as much an art form as business activity. On one side the question is will economic activity spur oceanborne freight… and from where? And on the other side, how many ships and in what sizes will be available to satisfy this demand? There is also the additional caveat that while understanding demand on principal or inbound leg may work, but matching this to another profitable leg is a challenge – inbound to China, then what?

From the shipowners’ perspective, an abundance of ships chasing freight equals lower rates, a nearly persistent condition since the crash of 2008.

Economists tend to look at the ships as “inelastic” supply, while industrial production is fluid, with many factors influencing demand. The thinking is the number of ships available for deployment is relatively fixed with adjustments from scrapping, layups (when necessary) and newbuilding additions.

With tepid GDP growth over the last few years, there has been little incentive for drybulk shipowners to invest in newbuildings in an overtonnaged market. Little fleet growth is expected in the short term.

But how right is the inelastic assumption? An under-appreciated aspect of ship capacity is speed. Similar to containership operators, dry bulk operators are also “slow steaming”. This means there is already excess capacity in the existing deployed ships and more elasticity then is generally acknowledged.

In December [2015] Peter Lindstrom, head of research for Oslo-based shipowner Torvald Klaveness, wrote in a ‘market outlook’ assessment for 2017:

“Take the example from the Panamax fleet which according to our monitoring has been running at around 11.4 knots lately. If freight increase enough to incentivize a speed increase (which also will be a function of bunker prices) then there is a latent supply increase through speed increase of about 16-17 percent if the fleet speed increases to e.g. 13.75 knots (assuming that 80% of the voyage days are at sea). Hence, if we experience some unforeseen demand shock then the potential of speed increases will slow down the pace of improvement in freight rates. So, while we do expect the demand growth to outstrip fleet growth in 2017 we can forget about the freight rates seen in the hay days prior to 2011.”Harbingers of Spring: Forecast 2017

John Baffes, Senior Economist and lead author of the Commodity Markets Outlook for the World Bank, wrote, “Prices for most commodities appear to have bottomed out last year and are on track to climb in 2017.” But like any good economist, he hedged his bets by saying, “However, changes in policies could alter this path.”

Of course, the “new policies” Baffes referring to are the raft of protectionist initiatives, which like the flu in a third-grade classroom could spread at every corner of the globe.

With the dry bulk orderbook and demolitions, there are minimal increases expected over the next couple of years to the dry bulk fleet. During the so-called anti or counter cyclical ship ordering from 2008-2013, as much as 25% of the total of the existing fleet was on order.

However, in this current down cycle, this amounts to the estimated 2 million in dwt deliveries in 2016 compared to 15 million dwt in 2015.

What does this mean in the near term for dry bulk shipping? Maybe not much in pricing. There is between 14%-18% in phantom fleet capacity in slow steaming and other under-utilization to soak up any market growth, especially in the projected 2.5%-3.3% range. In real terms, more volume but not improvement in the BDI.

Could the forecast change? Despite the uncertainty of today, crocuses and economists usually get it right. A little evidence of global economic stability and indeed a new spring could be at hand…or not.