There is no doubt China is key to the dry bulk sector. Reforms in steel making that began several years ago in China are now taking hold. But questions abound as to how the country’s steel industry restructuring will impact global dry bulk shipments.

China ore else what? When it comes to dry bulk demand forecasts, China’s always the key - and the key is made of steel.

Throughout the 1980s and into the 1990s, China’s economy annually posted double digit GDP growth (with some exaggeration in numbers) as China rode the “export model” to modernization. China’s industrial growth as transformation into the “world’s factory” was also the driver behind the rise in commodity movements, especially related to steel and steel products. Like the old adage a rising tide lifts all boats, the increase in commodity movements to China (and the export products created from those commodities) in turn has lifted the BDI, albeit from a very low starting point.

China is still the largest importer of iron ore and coal by a wide margin. For example, back in 2014, China imported a whopping 70% of the world’s iron ore and nearly 20% of the world’s coal. Even now there is a much closer correlation between the BDI and China’s imports than global GDP growth figures. Iron and steel remain the biggest market drivers.

Drewry, the London-based shipping research firm, wrote in the February edition of their Dry Bulk Forecaster, “Demand is projected to grow at a healthy pace of 3%...” but there are many ways this freight friendly forecast could get derailed, beginning with China.

The World Steel Association, better known as Worldsteel (a group representing 160 steel producers accounting for 85% of global production), wrote in their April appraisal, “We expect that Russia and Brazil will finally move out of their recessions. After the demonetization shock, the Indian economy is expected to resume growth.” “However, China, which accounts for 45% of global steel demand, is expected to return to a more subdued growth rate after its recent short uplift.”

Worldsteel is currently forecasting China’s demand for steel to be flat this year at 681 million tons and fall 2% next year to 667.4 million tons.

But Worldsteel boosted its estimate for last year’s demand growth to 1% from 0.2%, primarily because Beijing’s infrastructure stimulus has, at least for the moment (with a slowdown expected by the fourth quarter), increased China’s domestic steel demand. China’s crude steel output rose by 1.8% year-on-year in March to a record 72.0 million tons, the thirteenth consecutive month production has increased on an annual basis. China’s 201.1million ton steel production in the first quarter was up by 4.6% on the same period last year, which compares to a contraction of -3.2% in first quarter of 2016. How this added production plays out long term is difficult to predict, as downturn in domestic steel consumption could lead to a surge in steel exports – the very issue the Trump Administration has complained about. (see Peter Buxbaum’s article on page 2)

The potential export issue aside, there are a number of favorable signs.

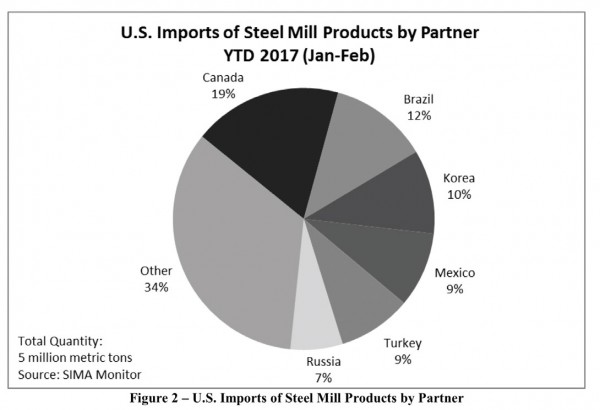

Iron ore imports are up. China Customs reports that the country imported 95.6 million tons of iron ore to China in March. Nearly 60 million tons came from Australia and just over 19 million from Brazil – respectively a year-on-year increase of 4.1 million tons and 1.4 million tons. Besides Australia and Brazil, other smaller suppliers have been exporting to China. For example, India exported 3.5 million tons in March, almost four times the amount a year ago. Iran also chipped in 2.5 million tons.

While it’s easy to focus on the major bulk commodities, a significant feature in the current rebound is the shipments of “minor” bulk commodities. For example, a nugget from the recent Custom data was China’s record import of 1.9 million tons of bauxite from Guinea in March which nearly doubled last year’s level. This puts bauxite to a four-month high of 5.1 million tons.

Zombie Mills and the Reverse Flow

There was a tremendous buildup of Chinese steelmaking capacity from 2010-2014, with production rising from 730 million tons in 2012 to peaking at 823 million tons in 2014. Much of the new capacity was SOEs (State Owned Enterprises) using induction furnaces (IF). China’s existing blast furnaces used relatively small amounts of scrap metal while the electric IFs use a much higher percentage. For example, in the US and Europe 50%-75% of the steel feeder stock is scrap. The scrap is highly processed before use. In China, the scrap metal has many impurities and the result is poor quality steel. But building the IFs was relatively easy and the domestic demand fed the steel plant building spree – notably many of the plants were producing rebar. When China’s housing demand tumbled, steel exports flooded the market, much to the consternation of US and European steelmakers. In a 2016 research report, investment banker Morgan Stanley noted, “According to data from the China Iron and Steel Association, an industry group, by November, 2015, some 48% of its member mills were loss-making.”

China’s “zombie” steelmakers have become a special target for restructuring under President Xi Jinping’s new economic policies.

Rachel Zhang, head of Morgan Stanley’s China materials equity research wrote, “China now has much lower tolerance regarding the survival of uncompetitive, low efficiency, and consistently loss-making SOEs.” Zhang believes 100 million tons of capacity could be taken off the books, ironically bringing production back into line with 2010/2011. Reports from China suggest that nearly 119 million tons have already been taken offline.

However, like the celluloid namesake, the Zombie steelmakers, while technically (outlawed) dead, refuse to die and continue to impact the market…in unexpected ways.

To hasten their demise, at the beginning of this year Beijing announced regulations, effective March 31st prohibiting the sale of scrap metal to IFs operators. Beijing surmised by removing the main feeder stock, the Zombie plants would eventually die. But much of the raw material for the plants was already stock piled.

While China has a 40% tariff on the export of ferrous scrap, tariff or not, dumping the scrap into the global market is one of the few business lines still open to the Zombie plants. With the domestic price of scrap around $180 per metric ton, exporting is simply a better alternative to local sale.

Sooner or later, the living dead steel plants will die.

But analysts’ have to wonder whether something similar will take hold in China during the next building boom and bust cycle?